NU’s Operational Excellence: A Crucial Element Behind Its Premium Story

NU Holdings: Efficiency Sets It Apart

While Nu Holdings (NU) is often categorized as a lender with a strong focus on credit, one metric distinguishes it from conventional banks: its efficiency ratio. This figure is becoming central to how investors view the company.

Impressive Growth and Customer Expansion

In the final quarter of 2025, NU achieved an impressive 45% increase in revenue compared to the previous year. The company also grew its customer base to 131 million, welcoming 17 million new users in a single quarter.

Efficiency Ratio: A Game Changer

The most notable development is NU’s efficiency ratio, which has dropped dramatically from 78% at the end of 2021 to just 20% recently. This means NU is able to generate revenue at a much lower cost than traditional banks. When compared to established institutions such as JPMorgan Chase (JPM) and Bank of America (BAC), NU’s cost structure is clearly more efficient.

Standing Out Among Fintechs

Even among digital banking peers like SoFi Technologies (SOFI), NU’s operational efficiency remains a key advantage. While SoFi benefits from a diverse, fee-driven business model, NU’s strength lies in its ability to keep costs low, allowing it to offer attractive pricing and still improve its profit margins.

Fintech Infrastructure Drives Growth

Although NU is sensitive to interest rate changes, it should not be mistaken for a traditional bank. Its technology-driven platform enables the company to scale up without a corresponding rise in expenses. This efficiency not only boosts earnings but also supports ongoing expansion.

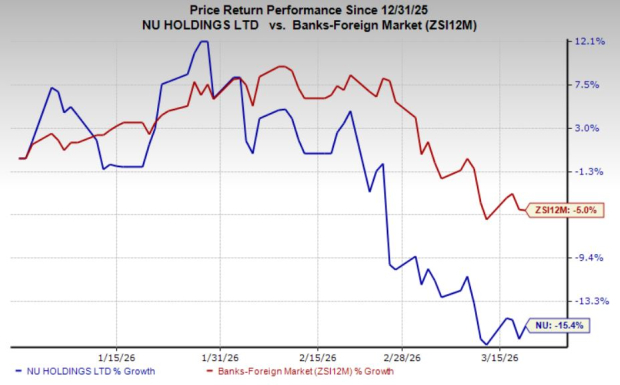

NU Stock: Performance, Valuation, and Analyst Outlook

So far this year, NU’s share price has fallen by 15%, compared to a 5% drop for the broader industry.

Image Source: Zacks Investment Research

In terms of valuation, NU trades at a forward price-to-earnings ratio of 15, which is significantly higher than the industry average of 9.97. The company has a Value Score of C.

Image Source: Zacks Investment Research

Analyst estimates for NU’s 2026 earnings have been trending upward over the past two months.

Currently, NU holds a Zacks Rank #2 (Buy).

Top Semiconductor Stock Opportunity

The surging need for data is driving a new wave of growth in the digital sector. As data centers are built and upgraded, companies supplying the necessary hardware are poised to become the next industry leaders, much like NVIDIA.

One lesser-known semiconductor company is well-positioned to benefit from this trend. It produces specialized chips that major players like NVIDIA do not, and is just starting to gain attention in the market—making now an ideal time to watch this stock.

Get More Stock Recommendations

Looking for more investment ideas? Download the "7 Best Stocks for the Next 30 Days" from Zacks Investment Research.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Dow, Nasdaq Near Correction After 4th-Straight Weekly Loss

Bitcoin Hyper Price Prediction: DeepSnitch AI Aims for 100x Post-Launch, While HYPER Can Only Deliver 2-3x