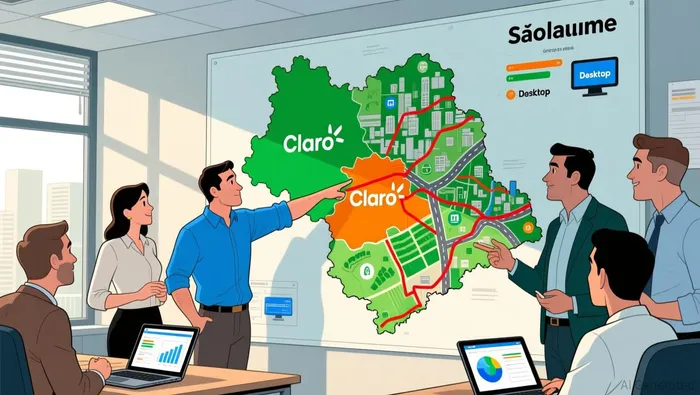

Claro's Desktop Bid Faces Regulatory Scrutiny as Market Waits for Price Breakthrough

Claro's pursuit of Desktop is a high-conviction, infrastructure-led move to correct a structural weakness in its Brazilian portfolio. The strategic driver is clear: to strengthen its fixed broadband business, which has been a weak segment amid a persistent decline in pay-TV subscriptions. Acquiring Desktop, the third-largest fiber broadband provider in São Paulo state, would directly bolster that underperforming unit and provide a critical mass of subscribers to accelerate its digital transformation.

The deal's scale underscores its ambition. If completed, it would give Claro over 50% market share in 66 cities, with a commanding 53% share in 20 key municipalities in São Paulo state. This concentration in a critical economic region represents a major step in consolidating Brazil's fragmented broadband market, a trend that analysts see as favorable for long-term industry efficiency and profitability.

Yet the transaction's path is currently stalled. Negotiations have slowed due to disagreements over contractual terms and pricing. Desktop's market cap sits at roughly $360 million, but a deal is expected to value it at over $400 million. This gap highlights the core tension: Desktop's owners seek a premium for their valuable fiber assets, while Claro must weigh that cost against the strategic benefits and the looming regulatory scrutiny that any such consolidation will trigger.

Financial and Competitive Impact

The acquisition would deliver a decisive, if concentrated, boost to Claro's Brazilian broadband footprint. Desktop's customer base is highly localized, with 51% of its 1.19 million broadband subscribers concentrated in 20 key cities in São Paulo state. For Claro, this represents a strategic infill play, directly addressing the weakness in its fixed broadband segment by adding a large, established customer base in a critical economic region.

| Total Trade | 12 |

| Winning Trades | 2 |

| Losing Trades | 6 |

| Win Rate | 16.67% |

| Average Hold Days | 0.83 |

| Max Consecutive Losses | 3 |

| Profit Loss Ratio | 1.69 |

| Avg Win Return | 11.35% |

| Avg Loss Return | 5.78% |

| Max Single Return | 13.66% |

| Max Single Loss Return | 8.45% |

This move, however, is a classic double-edged sword. While it strengthens Claro's competitive position against rivals like Telefonica Brasil, which had previously talked with Desktop, it simultaneously invites intense regulatory scrutiny. The transaction would create a dominant player in a specific geographic cluster, triggering the need for a detailed antitrust review by Brazil's Administrative Council for Economic Defense (CADE). Analysts note that any remedies or structural solutions would be defined within CADE's case-specific review, with Brazil's telecommunications agency (ANATEL) also assessing the deal from a competition perspective.

The competitive context adds another layer of complexity. The deal is not a straightforward take-private; it is a contested asset. The recent activity of small provider associations, which have intervened as interested third parties in other concentration cases, suggests the regulatory landscape is becoming more active. This means Claro's capital allocation decision is now entangled with a potential multi-month approval process, where the final terms could be dictated by regulators rather than the original negotiating parties. For an institutional investor, this introduces a significant execution risk that must be weighed against the clear operational benefits.

Catalysts, Risks, and Forward View

The deal's immediate catalyst is a resolution on price and terms. Despite ongoing talks, negotiations have slowed to a near standstill due to disagreements over contractual terms and pricing. Desktop's market cap is about $360 million, but a deal is expected to value it at over $400 million. This gap is the core uncertainty. The stock's sharp decline after the Reuters report underscores the market's view that the transaction is now "on hold" pending a price agreement. For institutional investors, this means the primary near-term event is a binary outcome: either the parties bridge this gap and announce a deal, or the talks dissolve, leaving Claro to reassess its infrastructure strategy.

The key risks are multifaceted. First, regulatory rejection due to market concentration is a material threat. The deal would create a dominant player in a critical economic region, triggering a detailed antitrust review by Brazil's Administrative Council for Economic Defense (CADE). Analysts note that any remedies would be defined within CADE's case-specific review, and the recent activity of small provider associations as interested third parties suggests a more active regulatory landscape. Second, Claro faces continued pressure on profitability from its currency mismatch. As a subsidiary of América Móvil, Claro's costs are largely in reais while its parent's financials are reported in dollars, creating a structural headwind that could amplify the impact of any regulatory or integration costs. Third, integration challenges are inherent in any consolidation, particularly when merging networks and customer bases in a fragmented market.

For institutional investors, this deal represents a high-conviction bet on infrastructure quality and market consolidation. It is a strategic move to correct a structural weakness in Claro's Brazilian portfolio, aiming to build a more resilient, high-margin broadband business. However, it requires a high tolerance for regulatory and execution risk. The capital allocation decision is now entangled with a potential multi-month approval process where the final terms could be dictated by regulators, not the original negotiating parties. This introduces a significant execution risk that must be weighed against the clear operational benefits. In the portfolio construction view, this is a sector rotation play within América Móvil's Latin American holdings, but it is a speculative one, dependent on navigating a complex and uncertain approval path.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

CZ's Response: Does It Indicate a Shift or Just Background Noise for Crypto Market Liquidity?

Hearts and Minds Encounters NTA Decline as Corporate Travel Impairment Highlights Exposure to Concentration Risk