FDA Grants Approval for Expanded Use of BMY's Opdivo in Treating Classical Hodgkin Lymphoma

Bristol Myers Squibb Expands Opdivo's Role in Cancer Therapy

Bristol Myers Squibb (BMY) has further solidified its position in oncology with recent regulatory green lights for Opdivo (nivolumab) in classical Hodgkin lymphoma (cHL) in both the United States and the European Union. These approvals highlight Opdivo’s growing significance in immunotherapy-driven cancer treatment strategies.

Opdivo is a fully human monoclonal antibody that targets the PD-1 receptor on T and NKT cells, functioning as a biologic therapy.

The U.S. Food and Drug Administration (FDA) has authorized the use of Opdivo in combination with doxorubicin, vinblastine, and dacarbazine (AVD) for adults and children aged 12 and older who have not previously received treatment for stage III or IV cHL.

This marks the first time an immunotherapy-based regimen has been approved as an initial treatment for this group, potentially establishing Opdivo as a new benchmark for advanced cHL care.

In Europe, the European Commission (EC) has approved Opdivo alongside brentuximab vedotin for certain pediatric and young adult patients with relapsed or refractory cHL after prior therapies. This decision introduces the first immunotherapy combination for this challenging treatment scenario, addressing a significant unmet medical need.

Opdivo is already available for adults with cHL that has returned or worsened after autologous hematopoietic stem cell transplantation (HSCT) and brentuximab vedotin, or after three or more lines of systemic therapy including HSCT. This use was granted accelerated approval based on overall response rates.

Recent Developments for Opdivo

The latest U.S. approval is supported by phase III SWOG 1826 trial data, which showed a 58% reduction in disease progression or death and a notable improvement in progression-free survival compared to standard treatments.

In Europe, the EC’s decision was based on phase II CheckMate-744 study results, which demonstrated effectiveness in patients with more difficult-to-treat relapsed disease.

These expanded indications increase Opdivo’s reach in both newly diagnosed and relapsed cHL, strengthen its competitive edge in blood cancers, and support long-term growth for Bristol Myers Squibb’s oncology division.

Opdivo is approved for a wide range of cancers, including those affecting the bladder, blood, colon, head and neck, kidneys, liver, lungs, skin (melanoma), pleura (MPM), stomach, and esophagus.

The combination of Opdivo and Yervoy is also approved in several countries for treating NSCLC, melanoma, MPM, RCC, CRC, HCC, and various gastric and esophageal cancers.

In 2025, Opdivo generated $10 billion in sales.

Bristol Myers Squibb’s Strategy Amid Shifting Drug Portfolio

In 2025, Bristol Myers Squibb maintained steady performance, thanks to robust sales from key products such as Opdivo, Opdualag, Reblozyl, Breyanzi, and Camzyos. These medicines have helped offset revenue declines from older drugs facing generic competition.

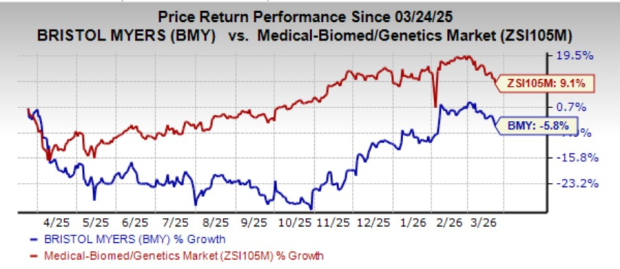

Over the past year, Bristol Myers Squibb’s stock has declined by 5.8%, while the broader medical and genetics industry has grown by 9.1%.

Opdivo, a leading immuno-oncology therapy, continues to drive the company’s cancer portfolio alongside Yervoy and Opdualag.

The FDA’s recent approval of Opdivo Qvantig (nivolumab and hyaluronidase-nvhy) for subcutaneous injection has further strengthened Bristol Myers Squibb’s immuno-oncology lineup. According to the company, this new formulation is expected to broaden patient access and extend the impact of Opdivo well into the future.

Looking forward, anticipated approvals for new therapies and expanded indications for existing drugs are expected to further diversify the company’s revenue streams.

BMY’s Stock Rating and Noteworthy Alternatives

Bristol Myers Squibb currently holds a Zacks Rank #3 (Hold). Other pharmaceutical and biotech companies with higher Zacks rankings include Liquidia Corporation (LQDA), ADMA Biologics (ADMA), and ANI Pharmaceuticals (ANIP). Both LQDA and ADMA have a Zacks Rank #1 (Strong Buy), while ANIP is rated #2 (Buy).

- Liquidia’s earnings per share (EPS) estimates have more than doubled to $1.75 in the last 30 days, with shares rising 65.9% over the past six months.

- ADMA’s projected 2026 EPS has increased from $0.85 to $0.96 in the past two months, although its stock has fallen 24.1% over the past year.

- ANI Pharmaceuticals’ 2026 EPS estimate has grown from $8.28 to $8.99 in the last 60 days, and its shares have climbed 13.1% over the past year. The company has surpassed earnings expectations in each of the last four quarters, with an average surprise of 22.21%.

Five Stocks with Doubling Potential

Each of these five stocks has been selected by a Zacks expert as a top candidate to potentially double in value over the next year. While not every pick will be a winner, previous recommendations have achieved gains of +112%, +171%, +209%, and +232%.

Many of these companies are still under the radar, offering investors a chance to get in early.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

BTR (Bitlayer) 24h amplitude 607.1%: Trading volume soars 718%, sell pressure leads to sharp drop

IBRX Soars 12% in Intraday Surge — What’s Fueling This Biotech Breakout?

Next Technology (NXTT) Plummets 24.5% Intraday – What’s Fueling the Sharp Decline?

Ubben Exits Bayer Stake as Smart Money Loses Confidence in Activist-Driven Turnaround