Playfair Mining's $2.16M Drilling Program at Nova Scotia's "Crumple" Site May Confirm a Hundred-Year-Old Gold Hypothesis Amidst Record High Prices

Playfair Mining Secures Major Funding for Mount Uniacke Exploration

Playfair Mining has successfully completed the first phase of its planned $2.4 million financing, raising $2.16 million through the sale of 35.9 million units at $0.06 each. These funds are allocated to support a focused exploration initiative at the company’s Mount Uniacke project in Nova Scotia. In preparation for this financing, Playfair recently streamlined its share structure, consolidating its outstanding shares from approximately 141 million to 47 million, enhancing its capital efficiency ahead of the new investment round.

The upcoming exploration campaign is designed to be both targeted and cost-effective. Management has detailed a 2,950-metre drilling program with a budget just over CAD$1 million. This initial effort will focus on three high-priority zones identified from a comprehensive review of 1,400 assessment reports, with special attention on the "Crumple"—a structurally complex, high-grade area that has seen little modern exploration. The goal is to test a geological hypothesis dating back a century, using current drilling methods to confirm its validity.

Strategically, Playfair aims to turn a speculative, high-potential target into real value, leveraging the current strength in gold prices. The company operates in a region that is attracting renewed investor interest, supported by record gold prices and favorable provincial policies. The recent capital raise provides the resources needed for this initial, low-risk test. However, as with all early-stage exploration, the outcome of this $2.16 million investment depends entirely on whether drilling results justify further development in today’s robust gold market.

Exploration Strategy: High-Grade Targets and Bulk Tonnage Potential

Playfair’s exploration plan is built around a three-part drilling program at Mount Uniacke, designed to evaluate two distinct geological models. The main focus is the "Crumple," a high-grade structural zone that has seen little drilling since geologist E.R. Faribault mapped it in 1901 and theorized it could host rich, untapped gold veins. A brief drilling effort in 1932 offered some support for this theory, but it has remained largely untested for decades.

The initial phase will involve drilling 600 metres at the West Lake Mine, aiming to confirm the presence of thickened gold veins at shallow depths, as predicted by the "Crumple" structure.

In parallel, Playfair will investigate the potential for a large, low-grade deposit near historic open cuts. This part of the program targets a different deposit style, inspired by evidence from a 1995 drill hole that returned 2.6 g/t gold from otherwise unremarkable core, suggesting the possibility of a high-tonnage, disseminated resource. This phase will include 1,550 metres of drilling, focusing on where the "Crumple" intersects a significant north-south vein system, roughly 850 metres from the well-documented West Lake Mine.

This exploration strategy is the result of extensive groundwork, including the review of 1,400 technical files to prioritize targets. Mount Uniacke emerged as the top candidate for both high-grade and bulk-tonnage exploration. The entire campaign is structured as a low-cost, proof-of-concept test, with the drilling budget capped at just over CAD$1 million. The project carries speculative risk, as its success depends on drilling results that could confirm a long-standing geological model. A positive outcome would lay the groundwork for further investment in a strong gold market, while a negative result would limit losses to a modest initial spend.

Gold Market Context: Historic Highs and Shifting Demand

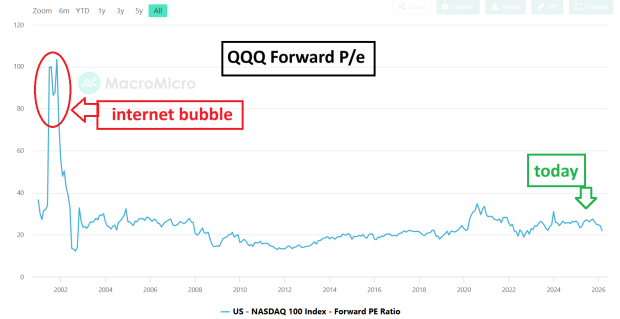

Playfair’s exploration efforts are set against a backdrop of unprecedented gold prices. This year, gold has climbed about 20%, reaching a record $5,594.82 per ounce in January. This surge is part of a multi-year rally, with gold appreciating over 64% in 2025 alone. The main driver is strong, structural demand, especially from central banks, which J.P. Morgan believes will continue to support prices. Investor demand, including from ETFs, has also been robust, averaging 585 tonnes per quarter in 2026.

Leading financial institutions remain optimistic about gold’s long-term prospects. J.P. Morgan recently increased its long-term price forecast to $4,500 per ounce, maintaining a 2026 year-end target of $6,300. The bank expects ongoing central bank and investor demand to push prices toward $5,000 by late 2026. Bank of America shares this outlook, suggesting gold could reach $6,000 within the next year. These projections are based on factors such as potential U.S. Federal Reserve rate cuts, geopolitical uncertainty, and continued demand for safe-haven assets amid currency volatility.

However, the market’s strength is accompanied by heightened speculative risk. Gold recently spiked above $5,600 per troy ounce before dropping sharply to $4,921 in a single week, erasing trillions in market value. This volatility highlights how quickly market sentiment can shift, especially after a 165% gain over two years. Analysts caution that the rally has become overextended, and corrections can be swift and severe, even in the context of strong long-term trends.

For Playfair, this environment offers both opportunity and risk. High gold prices enhance the value of any new discovery, but they also mean that expectations are high and the margin for disappointment is slim. The company’s low-cost, proof-of-concept drilling approach is a prudent way to proceed, balancing the potential for significant upside with limited financial exposure, while the broader market navigates the tension between sustained demand and speculative excess.

Key Catalysts, Risks, and Considerations

The core investment case for Playfair Mining centers on a single, near-term milestone: the results from its upcoming drill program. The company’s 2,950-metre, three-phase exploration effort is designed to test the high-grade "Crumple" target, with results expected later this year. A successful outcome would validate a century-old geological theory and provide a solid basis for further investment. If the results are disappointing, the company will have limited its losses to a relatively small initial outlay, but will be left with an unproven target.

Nevertheless, the broader gold market introduces additional risks that could impact Playfair’s prospects. The main concern is that much of the sector’s optimism may already be reflected in current prices, following a 165% rally over two years and a recent sharp correction. Analysts warn that the potential for further gains may be limited, especially for junior explorers. The recent volatility is a reminder that even strong long-term trends can be interrupted by sudden downturns.

Another significant risk is the sustainability of central bank demand, which has been a key driver of gold’s rally. While J.P. Morgan believes there is still room for further diversification into gold, recent price swings suggest that this demand could be nearing its peak. If central bank buying slows as prices rise, it could remove a major support for the market. Playfair’s low-cost, proof-of-concept approach is a sensible way to manage these uncertainties, but the company’s ultimate success remains closely tied to the health and direction of the gold market as a whole.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

The past indicates that the surge in AI still has potential to grow

Changes to Bank of Canada Governing Council

Stevens & Lee's Pittsburgh Bet: Strategic Signal or No Skin in the Game?

Kratos Selected by SKY Perfect JSAT as Strategic Partner for 5G NTN Satellite Ground System