EIA's Data Center Survey Sheds Light on the Overlooked Energy Issue Driving Regulatory and Financial Challenges

Challenges in Measuring Energy Use in Emerging Sectors

Regulators have consistently faced difficulties in accurately assessing the energy consumption of rapidly evolving industries. Historically, when new technologies disrupt the economic landscape, the absence of reliable data often persists. This was highlighted in 2018, when the U.S. Energy Information Administration (EIA) attempted to evaluate energy usage in data centers. Their findings emphasized the necessity for robust data collection frameworks and active industry collaboration for meaningful results. Today, this lack of information has become a significant obstacle as the sector expands.

Rising Electricity Demand and the Role of Data Centers

The United States is experiencing a resurgence in electricity consumption reminiscent of the growth seen before the 2000s. Back then, energy demand surged by as much as 30% due to the widespread adoption of new appliances and electronics. Now, advancements in artificial intelligence, increased manufacturing, and electrification are projected to push overall energy demand up by approximately 15-20% over the next ten years. Data centers are quickly becoming some of the largest new electricity consumers, with AI-related workloads driving usage faster than efficiency improvements can offset.

Bridging the Data Gap: Policy and Planning Implications

The longstanding delay in collecting accurate energy data has become a pressing policy issue. The EIA’s latest survey initiative is a crucial, albeit overdue, effort to address this gap. Without dependable information, energy planners are unable to make informed decisions about grid infrastructure or the true costs of transitioning to new energy sources. The lesson is clear: as sectors become major energy consumers, comprehensive data collection must follow.

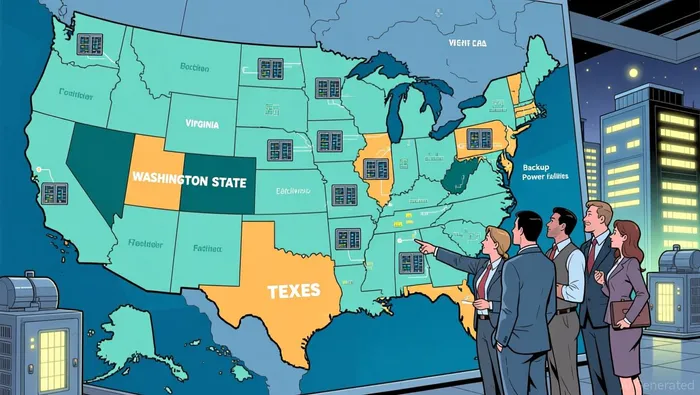

Inside the EIA’s Pilot Survey: Scope and Methodology

The EIA is launching its new survey with a focused approach, beginning with pilot studies in Virginia, Washington State, and Texas. This gradual rollout echoes the agency’s cautious strategy from 2018, when it concluded that high-quality data and industry participation were essential for credible outcomes. The measured pace is a direct response to previous challenges, such as the halted survey of cryptocurrency mining operations following legal pushback over privacy concerns.

The survey’s initial questions target critical operational and regulatory issues. Investigators will assess whether data centers have backup power systems and the types of fuels they utilize. This line of inquiry is vital, as a significant mismatch between utility delivery schedules and developer needs is prompting nearly one-third of developers to consider fully self-powered campuses by 2030. Understanding the extent and composition of backup power sources—ranging from natural gas and diesel to nuclear—will help evaluate the environmental and grid reliability impacts of distributed generation.

The EIA’s method prioritizes accuracy over speed, aiming to assemble a dependable, if patchwork, dataset before expanding to a nationwide survey. This deliberate process highlights the difficulty of overcoming years of missing data. The foundational questions being asked now will shape future regulatory decisions on power supply, emissions, and the evolution of the data center industry.

Regulatory and Financial Implications: Shifting the Cost Burden

The EIA’s survey is more than a data-gathering exercise—it is set to influence how the financial responsibilities for data center energy use are allocated. The results will inform new policies that seek to make technology companies directly accountable for their energy consumption, moving away from broad incentives toward models that require direct payment for power generation.

A prominent example is the "ratepayer protection pledge" announced by President Trump, which is expected to be formalized with leading tech companies. This policy mandates that tech firms fund their own power generation for new data centers, aiming to shield consumers from rising energy costs linked to unaccounted demand. Governors in the PJM region have pointed to poor grid management as a root cause of these issues. The survey’s findings will provide the evidence needed to enforce this “bring your own generation” approach.

This marks a broader regulatory shift. States are moving away from offering unconditional incentives and are instead holding large energy users responsible for their impact. For instance, Illinois has proposed a temporary halt to its data center tax incentives to address escalating electricity bills—a sharp departure from its previous policies. Meanwhile, states like Washington and Oregon are advancing legislation requiring data centers to finance necessary grid upgrades.

In response, companies are adjusting their strategies. Firms such as Meta and Google are securing clean energy through direct purchase agreements, aligning with new state requirements like Virginia’s renewable energy-linked tax exemptions. These agreements help mitigate regulatory and financial risks as the policy landscape evolves.

Ultimately, the longstanding lack of data is being addressed, ushering in a new era of financial accountability. The survey’s outcomes will substantiate the scale of energy demand, supporting policies that shift the costs of power generation from communities to the tech companies driving consumption. The period of unchecked grid expansion is coming to a close.

Key Developments and Future Trends

The transformation of the data center sector into a power-driven industry is now being tested by several emerging trends. The EIA’s survey is a pivotal first step, but its results will only begin the process of validating the true scale of demand—especially in states like Virginia and Texas, where the industry is most concentrated. The survey’s emphasis on backup power fuels will reveal how far developers are willing to go to secure reliable energy, a trend already evident in the growing gap between utility timelines and developer expectations.

Beyond the survey, the speed at which utilities connect new projects and the actual construction of onsite power facilities will serve as immediate indicators of industry direction. The adoption of advanced technologies like high-voltage central busways and DC distribution by 2028 demonstrates a commitment to efficiency, but also highlights underlying challenges. If delays in utility connections persist and more developers opt for fully self-powered campuses, it will confirm that grid expansion is lagging behind demand. Conversely, rapid progress in clearing connection backlogs and reduced onsite power planning would suggest a more optimistic outlook for grid investments.

Perhaps the most significant catalyst for change will be the implementation of policies such as the "ratepayer protection pledge". The upcoming White House meeting on March 4, 2026, where major tech companies are expected to endorse the pledge, marks a pivotal moment. The broader impact will depend on how quickly and widely these accountability measures are adopted at the state level. States like Illinois, Washington, and Oregon are already moving in this direction, and the pace of this transition will directly affect the financial outlook and investment strategies for data centers.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Canary Gold’s Drill Holes Signal Lateral Gold Continuity—Could This Junior Be the Trend’s Main Character?

FTSE 100 energy shares capitalize on oil price swings as geopolitical tensions drive sector rotation

Easter Shopping Booms Amid Slowing PMI: Retailers Face Challenges from Growing Expectation Discrepancy

Markets Grow Skeptical of Trump's Hormuz Forecast as Probability Drops Under 25%