PDD Holdings 2025 Q4 Earnings: Growth Significantly Slows, Full Bet on Supply Chain Investment to Build the "New Pinduoduo"

Bitget2026/03/25 13:02

Bitget2026/03/25 13:02Core Highlights

PDD Holdings (PDD) delivered steady revenue growth in Q4 2025, but net profit declined year-over-year and fell short of market expectations. Total revenue slightly exceeded analysts’ forecasts, primarily driven by strong transaction services performance, while profit pressure stemmed from continued investments in supply chain and ecosystem development. Operating cash flow decreased, yet cash reserves rose significantly. The company announced a RMB 100 billion investment over the next three years for supply chain infrastructure and officially established “New Pinduoduo” to advance self-owned brands and global supply chain integration. The stock reacted positively, rising approximately 1.91% on the day. Overall, short-term results faced pressure, but the long-term strategy focuses on supply chain upgrading.

Detailed Breakdown

- Overall Revenue and Profit Performance

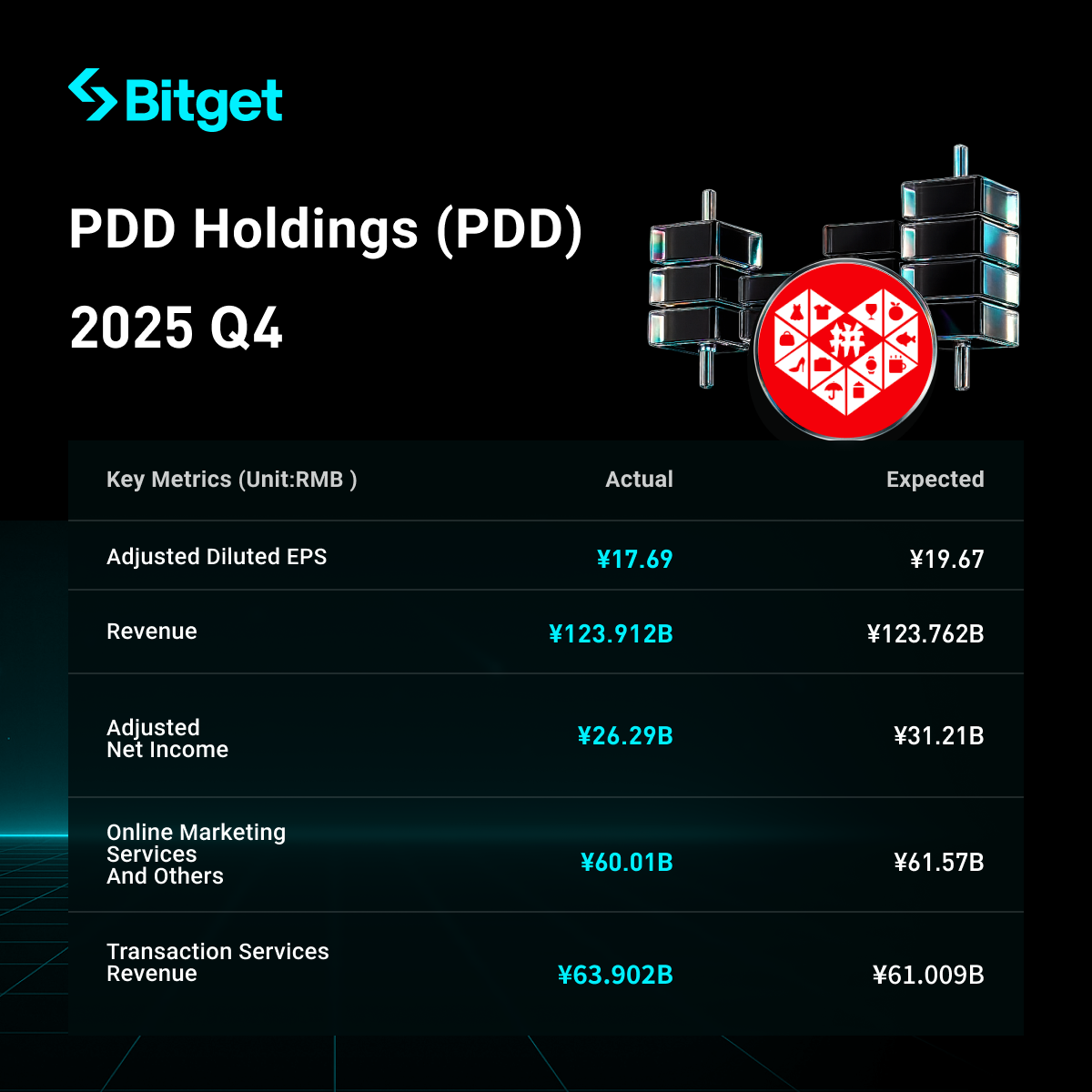

- Total revenue: RMB 123.912 billion (approx. USD 17.719 billion), up 12% YoY from RMB 110.610 billion in the prior-year period, slightly above market consensus of RMB 123.762 billion.

- Operating profit: RMB 27.720 billion, up more than 8% YoY from approx. RMB 25.592 billion.

- Net income attributable to ordinary shareholders: RMB 24.541 billion, down 11% YoY from RMB 27.446 billion.

- Non-GAAP net income attributable to ordinary shareholders: RMB 26.295 billion, down 12% YoY and missing consensus estimate of RMB 31.210 billion.

- Earnings per share (EPS): Basic EPS RMB 17.50 (prior-year RMB 19.76); diluted EPS RMB 16.51 (prior-year RMB 18.53); adjusted diluted EPS RMB 17.69 (prior-year RMB 20.15).

- Net cash from operating activities: RMB 241.195 billion (prior-year RMB 295.472 billion).

- Cash and cash equivalents plus short-term investments: RMB 422.3 billion (approx. USD 60.4 billion) at year-end, significantly higher than RMB 331.6 billion at the end of the previous year.

- Core Business Performance

- Online marketing services and other revenues: RMB 60.010 billion (approx. USD 8.581 billion), up 5% YoY.

- Transaction services revenue: RMB 63.902 billion (approx. USD 9.138 billion), up 19% YoY — the primary driver of overall revenue growth.

- Other Business Segment Performance (The report does not provide further breakdown of individual segments such as international business Temu. Revenue is mainly presented in two categories: online marketing services and transaction services. Overall growth was led by transaction services, while slower growth in marketing services may reflect intensified competition.)

- Future Plans: Supply Chain Investment and “New Pinduoduo” Establishment

- The company is fully committed to supply chain development and has officially formed “New Pinduoduo” to integrate supply chain resources across Pinduoduo and Temu, incubate self-owned brands, and target the global market.

- A new special-purpose company was established in Shanghai with an initial cash injection of RMB 15 billion.

- Planned total investment over the next three years: RMB 100 billion, aimed at systematically operating brands across different markets and categories, and upgrading “Made in China” to higher value chains.

- CEO Chen Lei emphasized adherence to long-termism and greater resource commitment to stakeholders; Co-CEO Zhao Jiashun noted that 2026 marks the start of the next decade and supply chain investment is a core commitment; CFO Liu Jun pointed out that continued exploration and investment amid changing external conditions will impact short-term financial performance.

- Next Quarter Guidance (No specific revenue or operating income guidance for Q1 2026 or the full year was disclosed. The company stressed that future results may fluctuate due to ongoing investments and that the current quarter’s profit should not be viewed as indicative of future performance.)

- Market Background and Investor Concerns

- Core Tension: Steady revenue growth (driven by transaction services) versus declining profit (due to increased investments). Non-GAAP net profit declined both year-over-year and significantly missed expectations, reflecting higher spending on supply chain, R&D, and ecosystem support.

- Market Challenges: Rapidly evolving competitive landscape, changing consumer demand, and global regulatory pressures.

- Investor Reaction: Despite the profit miss, revenue slightly beat expectations and the announcement of a massive supply chain investment plan elicited a positive market response, with PDD shares rising 1.91% on the day. Investors are mainly concerned about short-term profitability being pressured by investments, but acknowledge the long-term strategic value of supply chain upgrading.

Disclaimer: This article is for reference only and does not constitute any investment advice.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Immix Biopharma: The $450 Million Valuation Discrepancy Shrinks as BLA Milestone Approaches

Arista Networks Sparks a Rally: The 3% Jump That Defied the Day’s Lowest Point

Meta's 600 Call Barrier: How the 575 Put Base Indicates a Tactical Recovery Opportunity

AMZN Options Flashpoint: What the $215 Call Barrier Reveals About an Imminent Breakout Attempt