India’s LPG imports are under pressure as the closure of the Hormuz Strait leads to expensive and uncertain alternative routes

Indian LPG Imports Face Severe Disruption Despite Limited Progress

Earlier this week, two Indian-flagged LPG carriers, the Jag Vasant and Pine Gas, successfully navigated the Strait of Hormuz, marking a tactical achievement for India. This event demonstrates that, with diplomatic efforts, safe passage is possible for select vessels. These tankers followed two others that completed the same route earlier in the month, suggesting a partial workaround for a waterway that has been largely inaccessible since late February.

However, this limited breakthrough pales in comparison to the broader supply crisis. In March, India’s total LPG imports are projected to reach only 1.19 million tonnes, a sharp decline. The shortfall is most pronounced from West Asia, which typically supplies the majority of India’s LPG. For the week ending March 19, West Asian shipments dropped to just 89,000 tonnes, the lowest since January. That week, total imports fell to 265,000 tonnes, with the US stepping in to partially offset the deficit.

Ultimately, while these successful transits show that some routes remain open, they account for only a small portion of the overall supply gap. The situation highlights shifting logistics rather than a true resolution to the ongoing crisis.

Absolute Momentum Long-Only Strategy: Overview and Performance

This trading approach involves taking long positions in SPY when the 252-day rate of change is positive and the closing price is above the 200-day simple moving average (SMA). Positions are exited if the price drops below the 200-day SMA, after 20 trading days, or if either an 8% profit target or a 4% stop-loss is reached.

Key Backtest Parameters

- Entry Criteria: 252-day rate of change > 0 and close > 200-day SMA

- Exit Criteria: Close < 200-day SMA, after 20 days, or upon reaching +8% profit or −4% loss

- Asset: SPY

- Risk Controls: 8% take-profit, 4% stop-loss, 20-day maximum holding period

Backtest Results

- Total Return: 2.77%

- Annualized Return: 1.4%

- Maximum Drawdown: 2.65%

- Win Rate: 0.55%

Trade Statistics

- Total Trades: 183

- Winning Trades: 1

- Losing Trades: 0

- Average Hold Days: 0.1

- Profit/Loss Ratio: 0

- Average Winning Return: 2.77%

- Average Loss Return: 0%

- Maximum Single Trade Return: 2.77%

- Maximum Single Loss: 0%

Supply-Demand Pressures Intensify in India's LPG Market

India’s LPG sector operates with little margin for error. Domestic output satisfies only 40% of national demand, leaving the country reliant on imports for the remaining 60%. This structural reliance has been exposed by the current crisis. Demand surged to a record 2.8 million tonnes in February, up 10% year-over-year, largely due to the government’s extensive LPG connection drive. The closure of the Strait of Hormuz has abruptly severed the main supply route, blocking about 90% of incoming shipments.

The immediate result is a dramatic supply shortfall. March’s imports are estimated at 1.19 million tonnes, a 46% drop from the previous month. India has been forced to rapidly diversify its sources, with US shipments now overtaking those from the Gulf. However, US cargoes take around 45 days to arrive, compared to just over a week from the Gulf, creating inventory gaps and logistical headaches. Russia and Argentina have also increased exports to India, but their capacity is limited and not well-suited for large-scale replacement.

In this context, the recent passage of two Indian tankers is a minor adjustment rather than a solution. The market is now contending with a more expensive and less predictable supply chain, underscoring India’s vulnerability due to its heavy import dependence.

Economic and Policy Repercussions

The strain on India’s LPG market is now evident in both statistics and daily life. The government has responded by raising the price of a standard 14.2-kg cylinder by ₹60 earlier this month, pushing prices in major cities like Delhi and Mumbai to record highs of around ₹913 and ₹912.50, respectively. Although prices have stabilized recently, the increase reflects ongoing cost pressures.

The impact extends to distribution networks. Companies such as Indane have introduced a WhatsApp-based refill booking service to better manage demand amid shortages. This digital shift is a direct response to operational challenges and aims to streamline a now more complicated supply process.

Subsidies, which help shield households from price shocks, are also under strain. The government covers up to 12 cylinders per household annually, with any additional purchases subject to volatile market rates. As international LPG prices surge, the cost for families exceeding the subsidy limit has become a significant burden.

These developments—rising prices, distribution adjustments, and tighter subsidies—are all symptoms of a deeper supply-demand imbalance. The market’s attempts to adapt are proving costly and disruptive for both consumers and businesses.

Key Risks and Future Outlook

The stability of India’s LPG supply now depends on several critical factors. The foremost risk is how long the Strait of Hormuz remains closed; a prolonged shutdown could further reduce imports, and alternative suppliers may not be able to compensate quickly enough for the lost Gulf volumes.

One potential turning point is the arrival of Iranian LPG shipments. The first cargo is expected this week, with more to follow. These regional supplies offer a faster alternative to the lengthy US route, but their reliability and scale are still uncertain. While Iran has indicated it will allow vessels from friendly countries, the actual quantities India can secure will depend on finalized agreements and the safe movement of ships out of conflict zones. The government’s recent purchase of an Iranian cargo is a positive sign, but it is only a small step toward addressing the deficit.

Another challenge is whether the US can maintain its current export pace. Indian oil companies aim to import 2.2 million tonnes of LPG from the US in 2026. While US shipments now exceed those from the Gulf, sustaining this flow throughout the year is uncertain. The lengthy transit time and any disruptions in US supply could quickly exacerbate shortages.

India is also seeking to diversify its suppliers, exploring long-term contracts with Norway, Canada, and Russia. The effectiveness of these efforts will depend on securing firm agreements that guarantee stable volumes, but for now, the market relies on short-term fixes and diplomatic maneuvers.

In summary, India’s LPG outlook will be shaped by the consistency of Iranian shipments, the ability to sustain high US import volumes, and the successful negotiation of new long-term supply contracts. Until these factors are secured, the risk of further supply disruptions remains elevated.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

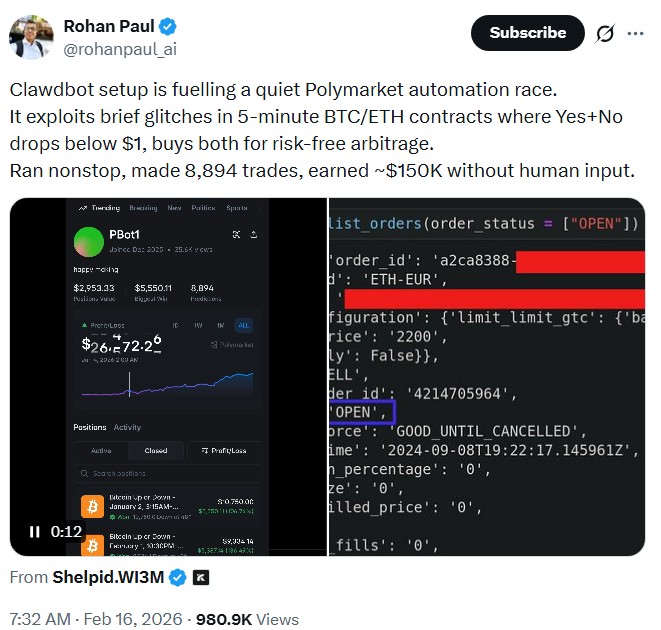

How AI agents can reshape arbitrage in prediction markets

XRP Global Distribution Shows The Major Holders And What It’s Being Used For

Vanguard VCR’s 40% Amazon-Tesla Bet Risks Derailing Its Consumer Discretionary Hedge Role

Meet the Value Stock With a 6.6% Dividend Yield That's Begging to Be Bought in April