CTA ammo is exhausted and positions are overheated! On the eve of tech giants’ earnings reports, Goldman Sachs warns of a stock market correction

According to Zhitong Finance, John Flood, a senior executive from Wall Street financial giant Goldman Sachs, stated that as U.S. and even global stock market positioning becomes increasingly crowded, and as the strong buying force of one of the key institutional forces—CTA—is about to turn into selling, equity market investors should be prepared for a certain degree of pullback in the short term.

Therefore, ahead of the consecutive earnings releases this week from the five major tech giants like Google, Microsoft, and Apple, Goldman Sachs strategists, including Flood, are warning that CTA marginal buying is drying up, pension fund rebalancing at month-end will bring selling pressure, hedge funds are deleveraging, and breadth indices continue to deteriorate—all these factors could collectively trigger a short-term pullback. However, the Goldman Sachs strategy team emphasizes that the medium- to long-term bull market outlook for equities remains intact, and any pullback is instead a significant buy-the-dip/opportunity to allocate into equities at lower levels.

This Goldman Sachs partner and head of Americas Equities Execution Services noted in the latest research report that the S&P 500 is expected to continue to rally significantly before the end of this year, but he is issuing a warning signal about a potential short-term sudden sell-off in this benchmark index. However, in this report dated Sunday, he also stated this should be viewed as a major buying opportunity on the dip.

From the AI bull run to overheated positions, Goldman Sachs sounds the correction alarm! But emphasizes a drop is a buying opportunity

The latest market forecast from the Goldman Sachs strategists is not that the “bull market is over,” but that the AI investment frenzy has driven short-term surges that are too intense, positions are crowded, and marginal buying is fading, making U.S. and global risk assets prone to a pullback. But this correction is more likely to be a rebalancing within a bull market, rather than a shift to a bear trend. John Flood and other strategists clearly point out that after buying about $53 billion over the past month, CTAs are no longer marginal buyers, month-end pension fund rebalancing could cause over $25 billion in U.S. equity selling, and hedge funds are deleveraging during the rebound. Still, he expects the S&P 500 to be “significantly higher” by year-end and defines any potential correction as a buying opportunity.

Systematic strategy funds—CTAs, also known as “fast money” flows, are likely to become a key selling catalyst. The Goldman team led by Flood reports that after buying about $53 billion worth of equity assets over the last month, Commodity Trading Advisor (CTA) funds now have about $32 billion in long positions on the S&P 500, and may not be the main buyers in the short-term. According to Goldman’s trading desk models, as the market becomes more range-bound, they may temporarily turn to selling; if stocks fall, the sell-off will intensify.

Massive month-end pension fund rebalancing is also expected to weigh on U.S. and global equity markets. The Goldman team led by Flood predicts that pension funds may sell over $25 billion worth of U.S. equities, which would make this potential selling one of the 15 largest monthly sell estimates since 2000.

“Excluding quarter-end dates—which include both monthly and quarterly rebalancing—this will be the largest monthly sell estimate ever,” added Flood and his team of strategists.

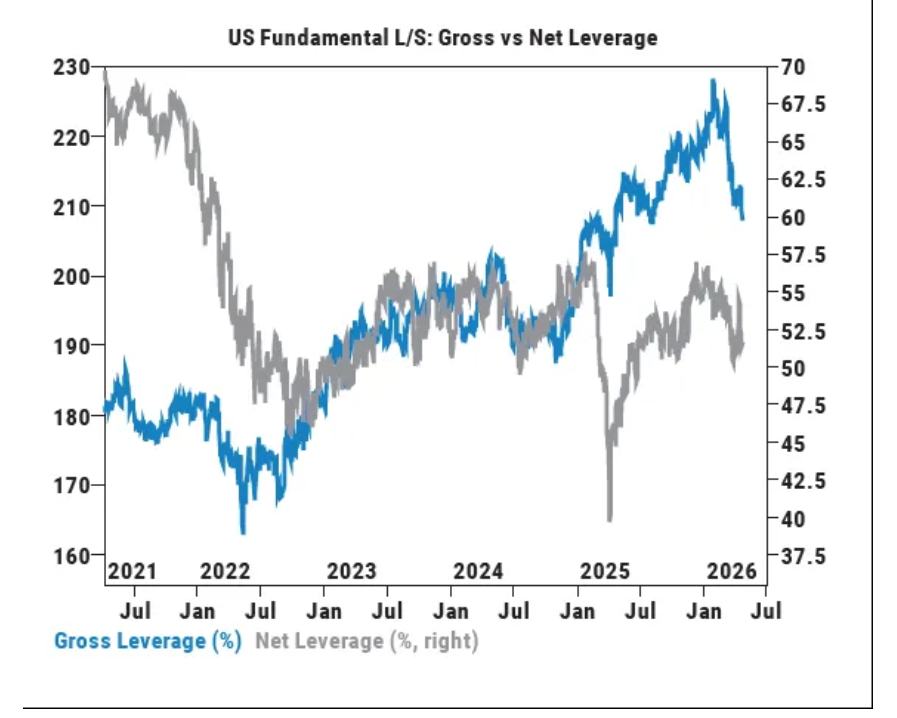

Meanwhile, in the hedge fund space, as managers aggressively covered short hedges during the recent rebound, overall leverage has dropped sharply. Goldman Sachs’ prime brokerage data shows overall trading activity fell last week for the first time in 13 weeks, indicating that leveraged hedge funds may have little room left to buy equities in the near term.

According to the firm’s statistics, hedge funds used the U.S. market rally to cut risk, trimming their gross long and short equity exposure to the largest reduction since September last year.

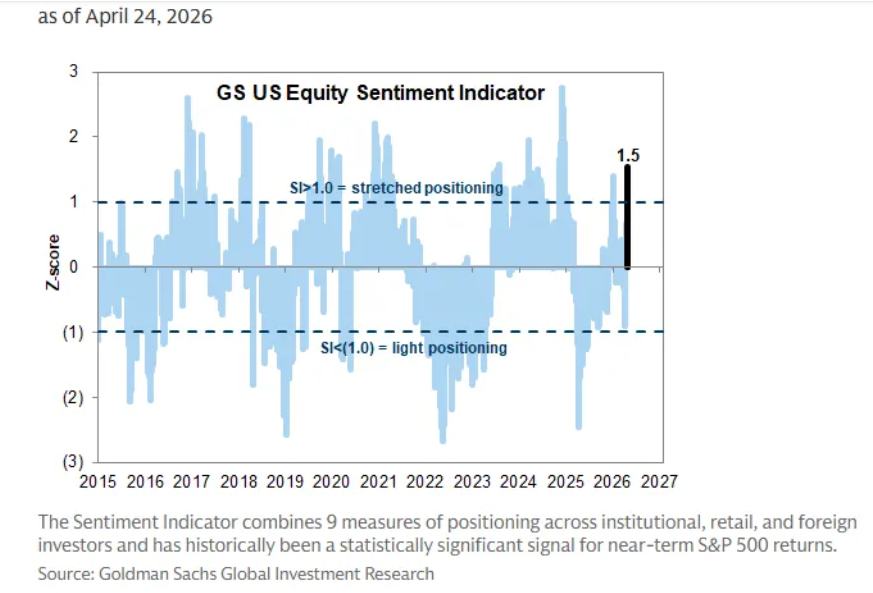

As of Tuesday’s U.S. market close, the S&P 500 and Nasdaq 100 took a breather, pulling back sharply from record highs after a substantial April rally. Supported by resilient corporate earnings and easing U.S.-Iran tensions, these two benchmark indexes are still on course for their strongest monthly performances in years. Rapid gains have pushed key indices into overbought territory and sharply increased investor exposure. The Goldman Sachs U.S. Equity Sentiment Indicator has also reached levels signaling crowded positioning.

Meanwhile, market breadth metrics have deteriorated significantly. The Philadelphia Semiconductor Index, known as the “semiconductor bellwether,” posted a record 18-day winning streak, and the gap between the S&P 500’s 52-week high and the median constituent’s 52-week high is at one of the widest since 2020—highlighting how concentrated the recent rally has been in AI computing power leaders such as Intel, AMD, Broadcom, and Micron. This makes equities more susceptible to any reversal, especially as in the next few days, some of the world’s largest technology giants—Google (GOOGL.US), Microsoft (MSFT.US), Amazon (AMZN.US), Facebook parent Meta (META.US), and Apple (AAPL.US)—will all announce their latest quarterly results.

Don’t chase the most crowded and overheated areas—investors’ best short-term entry point may soon appear on a pullback

More precisely, Goldman Sachs is concerned about a highly volatile earnings season for the five tech giants, combined with large-scale CTA/pension fund selling pressure, overheated semiconductor stocks closely tied to AI computing infrastructure, and oil/interest rate pressures, all of which, if U.S.-Iran tensions persist, could act as negative catalysts and trigger a short-term “technical/positioning-driven pullback.” But over the medium term, as long as AI capital expenditure, corporate earnings, share buybacks, and tech giant cash flows remain robust to support fundamentals, Goldman Sachs still tends to believe the main trend remains upward within a bull market framework.

Reportedly, the latest stance of Goldman Sachs’ head of hedge fund sales, Tony Pasquariello, is similar to that of senior executive John Flood: the bull market is far from over, but it’s not the time to chase highs, nor is it worth going short; rather, it’s better to maintain core long exposure while waiting to deploy capital after a pullback. In other words, Goldman Sachs is not calling for a retreat but is warning investors: don’t chase the hottest, most crowded trades; at least in the short term, the real entry point for equities may emerge with a coming pullback.

Tony Pasquariello underscores the localized “blow-off top” risk in tech and semiconductors. The Philadelphia Semiconductor Index’s single-month surge, sky-high RSI technical readings, and the extreme deviation relative to the 200-day moving average—all indicate the AI computing chain’s right-tail narrative has been rapidly and disproportionately priced in, even with a short-squeeze flavor. The key issue here is not a lack of AI demand, but that in the short term, the market’s trade that “AI CapEx is continually revised up, and semiconductor profits are endlessly extended” has become overly crowded. The Goldman Sachs U.S. Equity Sentiment Indicator has risen to a level reflective of tight positioning—a reading that, historically, often precedes pressured returns in the following weeks. With tech giants’ earnings clustered and worsening market breadth, the rally increasingly relies on a few large AI stocks, naturally reducing the market’s short-term risk tolerance.

Rich Privorotsky, head of Goldman Sachs Delta-One, issued a macro warning from the combination of oil prices and interest rate pressures. If the Iran situation fails to normalize quickly, the oil shock would not merely be a one-off event, but would transmit continuously through gasoline, shipping, inflation expectations, corporate costs, and nominal rates. Goldman Sachs has already raised its Q4 Brent crude forecast to $90–100 per barrel and, in extreme scenarios, is even discussing higher oil price risks—signaling that the energy market is repricing for the persistence of conflict. If oil remains elevated, it becomes harder for the Federal Reserve to turn dovish rapidly, and yields on 10-year and longer-dated Treasuries also come under more pressure, directly challenging high-valued tech stocks’ discount rate assumptions.

From an investment strategy perspective, the AI computing power bull narrative is not over, but this earnings season is a “ROI-verification moment,” not a “victory celebration.” The broader direction for AI investments remains long, but the real shift is that capital will continue to pivot from generic AI concepts toward the hardest, tightest, and most commercially clear segments in cloud computing power orders. Whether the global equity bull market continues depends on whether the five tech giants simultaneously present three clear expansion tracks: sustained strong AI CapEx, increasingly defined AI-related revenue realization paths, and no loss of profit margin/cash flow discipline.

Morgan Stanley’s logic matches Citibank’s: the first sign for judging AI investment returns is a revenue acceleration from AI-related businesses, not simply the scale of AI CapEx; that is, whether these $1 trillion-plus giants can persistently maintain an aggressive AI infrastructure investment cycle, driven by the growing clarity of AI monetization/growth paths. Google must prove its cloud computing business and cloud AI-related revenues can absorb depreciation pressure; Microsoft must prove Azure compute demand still exceeds supply; Meta must show that AI-driven ad cash flow growth is enough to cover its AI infrastructure expansion; and Amazon must prove the credibility of AWS big customer commitments and AI infrastructure capacity realization paths for 2027–2028. Meanwhile, another Wall Street giant, JPMorgan, has already raised its S&P 500 year-end target to 7,600 points, precisely because of AI-driven earnings upgrades and tech sector momentum, indicating that mainstream Wall Street capital still leans toward the AI trade not being over yet.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

USD/INR extends its advance as oil prices rise further

NAORIS (NAORIS) fluctuates 40.3% in 24 hours: trading volume surges as price breaks through consolidation range