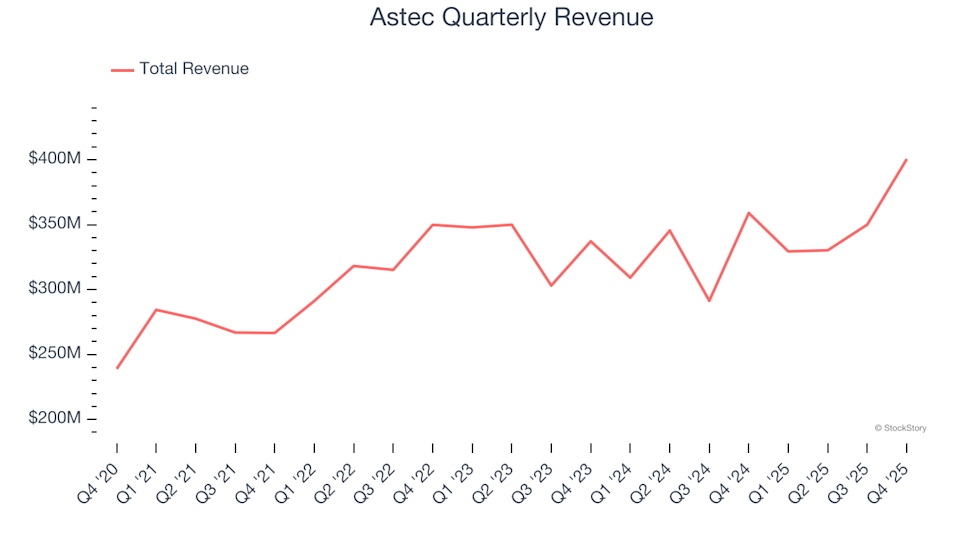

Astec (NASDAQ:ASTE) Surpasses Projections with Robust Q4 Results for Fiscal Year 2025

Astec (ASTE) Q4 2025 Earnings Overview

Astec, a leading provider of construction equipment (NASDAQ:ASTE), delivered fourth-quarter 2025 results that surpassed market expectations. The company reported revenue of $400.6 million, representing an 11.6% increase compared to the same period last year. Adjusted earnings per share reached $1.06, exceeding analyst forecasts by 27.7%.

Q4 2025 Highlights

- Revenue: $400.6 million, beating the $374.2 million consensus (11.6% year-over-year growth, 7.1% above estimates)

- Adjusted EPS: $1.06, compared to the expected $0.83 (27.7% above estimates)

- Adjusted EBITDA: $44.7 million, outpacing the $37.5 million forecast (11.2% margin, 19.2% beat)

- Operating Margin: 5.7%, a decrease from 12.2% in the prior year’s quarter

- Free Cash Flow Margin: 1.8%, down from 8.9% a year ago

- Backlog: $514.1 million at quarter-end, up 22.5% year-over-year

- Market Cap: $1.34 billion

About Astec

Astec (NASDAQ:ASTE) is known for pioneering the double-barrel hot-mix asphalt plant and supplies equipment for road construction, material processing, and concrete production.

Revenue Trends

Evaluating a company’s performance over several years helps reveal its true quality. While any business can have a strong quarter, sustained growth is a better indicator of long-term strength. Over the past five years, Astec’s annualized revenue growth was 6.6%, which is modest for the industrial sector and falls short of our preferred benchmark.

We prioritize long-term growth, but it’s important to recognize that five-year trends may overlook industry cycles or the impact of new contracts and product launches. Recently, Astec’s revenue growth slowed to an annualized 2.7% over the past two years, trailing its five-year average. This deceleration, common among construction machinery companies facing cyclical challenges, signals potential shifts in market demand. Still, Astec outperformed many of its peers during this period.

Examining the company’s backlog—orders yet to be fulfilled—offers additional insight. Astec’s backlog stood at $514.1 million at the end of the quarter, but it has averaged a 13.1% annual decline over the past two years. Since backlog growth lags behind revenue growth, the company may struggle to sustain its current pace going forward.

Recent Performance and Outlook

This quarter, Astec achieved 11.6% year-over-year revenue growth, with sales surpassing Wall Street’s projections by 7.1%.

Looking ahead, analysts anticipate revenue to rise by 3.6% over the next year, in line with the recent two-year trend. This forecast suggests that new offerings are unlikely to drive significant top-line acceleration in the near term.

As technology continues to transform every industry, the demand for developer tools—ranging from cloud monitoring to seamless content streaming—remains strong.

Profitability and Margins

Operating margin is a key indicator of profitability, reflecting how much profit remains after covering production, sales, and R&D costs. Over the past five years, Astec maintained profitability, but its average operating margin of 5.1% was relatively low for an industrial company, largely due to a modest gross margin.

On a positive note, Astec improved its operating margin by 5.1 percentage points over the last five years, benefiting from increased sales and operational leverage.

In the latest quarter, operating margin was 5.7%, down 6.5 percentage points from the previous year. This decline suggests higher spending on marketing, research, and administrative functions relative to gross profit.

Earnings Per Share (EPS) Analysis

While revenue growth shows how a company expands, changes in earnings per share (EPS) reveal whether that growth is profitable. Astec’s EPS has increased at a compound annual rate of 10.4% over the past five years, outpacing its revenue growth and indicating improved profitability per share.

Examining shorter-term trends, Astec’s EPS grew at an 11.2% annualized rate over the past two years, consistent with its five-year performance and demonstrating stable earnings power.

In Q4, adjusted EPS was $1.06, down from $1.19 a year earlier, but still comfortably ahead of analyst expectations. Wall Street projects full-year EPS of $3.29 for the next 12 months, which is roughly flat year-over-year.

Summary and Investment Considerations

Astec’s latest results were encouraging, with both EPS and EBITDA surpassing market forecasts. The stock responded positively, rising 1% to $59.09 after the announcement.

While the quarter was strong, a single earnings beat does not guarantee long-term investment success. It’s important to weigh these results against the company’s overall quality and valuation before making a decision.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

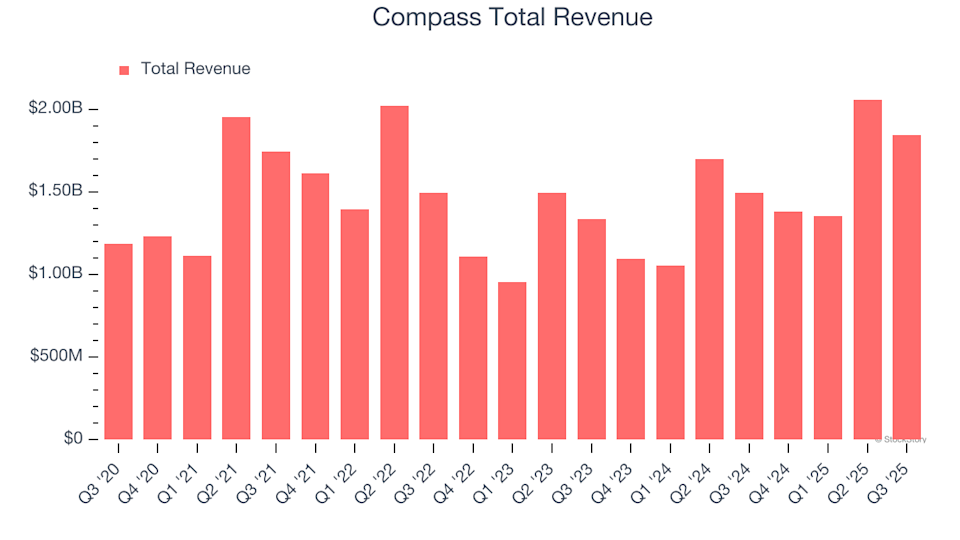

Earnings To Watch: Compass (COMP) Will Announce Q4 Results Tomorrow

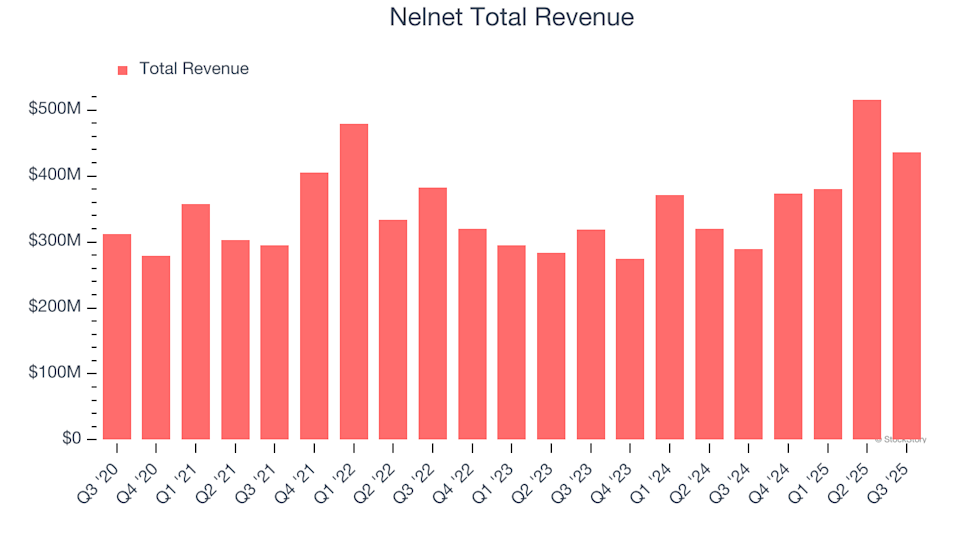

Nelnet (NNI) Q4 Preview: Key Information Before Earnings Release

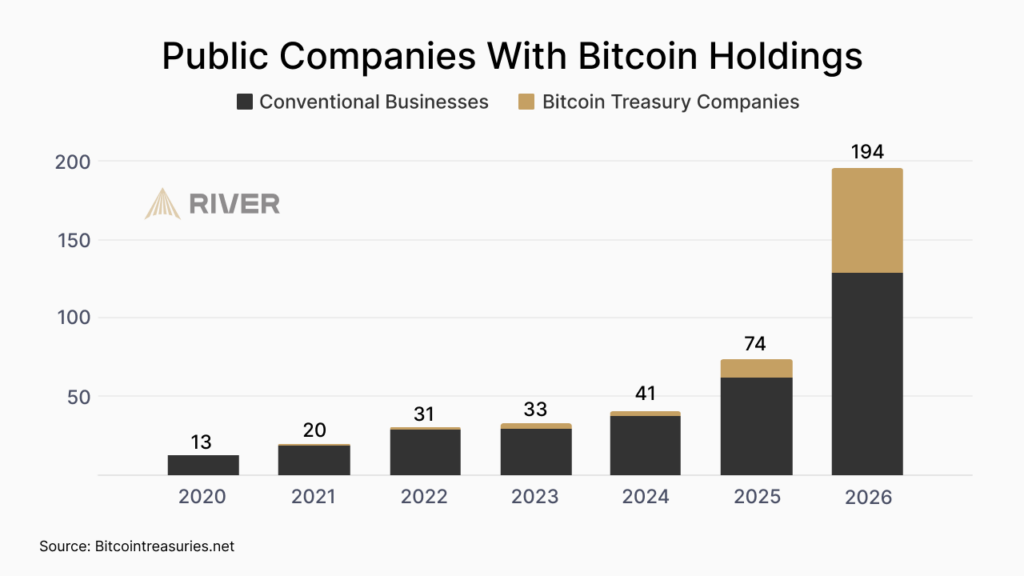

Bitcoin Gains Global Ground Despite Stagnant Valuation