Should You Consider Including AES Stock in Your Portfolio Ahead of the Q4 Earnings Announcement?

AES Corporation Set to Announce Q4 2025 Results

AES Corporation is scheduled to release its fourth-quarter 2025 financial results on February 26, after the market closes. Analysts anticipate earnings of $0.62 per share, which would represent a 14.81% increase compared to the same period last year. Revenue is projected to reach $3.49 billion, reflecting a 17.83% year-over-year gain.

Review of AES’ Recent Earnings Surprises

Over the past four quarters, AES has exceeded earnings expectations twice and fallen short twice, resulting in an average earnings surprise of 14.68%.

Quantitative Model Outlook

Current quantitative analysis suggests AES is likely to surpass earnings estimates this quarter. The combination of a positive Earnings ESP (+0.54%) and a Zacks Rank of #2 (Buy) increases the probability of an earnings beat.

Recent Utility Sector Earnings

- CenterPoint Energy, Inc. (CNP): Reported adjusted earnings of $0.45 per share for Q4 2025, missing consensus by $0.01 but improving 12.5% from the prior year’s $0.40.

- Duke Energy Corporation (DUK): Posted Q4 2025 earnings of $1.50 per share, slightly below the expected $1.51 and down 9.6% from $1.66 a year earlier.

Key Factors Influencing AES’ Q4 Performance

AES is expected to have benefited from ongoing investments in modernizing infrastructure and strengthening grid reliability, which have improved operational performance. Robust sales, continued cost management, and positive returns from renewable and utility operations likely contributed to quarterly growth.

Rising electricity demand from data centers, fueled by artificial intelligence applications, may have further supported earnings. Favorable regulatory rate decisions in previous quarters could have bolstered regulated revenues and helped offset inflationary pressures. Additionally, new projects likely began contributing to revenue for the full quarter.

However, warmer-than-average temperatures in most service areas during October to December may have reduced the need for heating, potentially impacting top-line results.

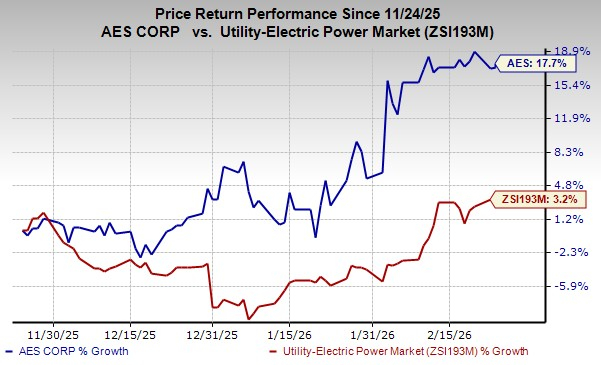

AES Stock Performance Overview

Over the last three months, AES shares have climbed 17.7%, significantly outpacing the utility-electric power industry’s 3.2% gain.

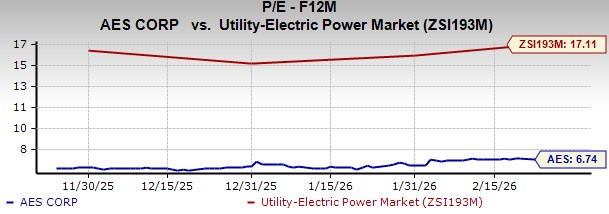

Valuation: AES Trading Below Industry Average

AES currently trades at a lower forward 12-month price-to-earnings ratio compared to its industry peers, suggesting a discounted valuation.

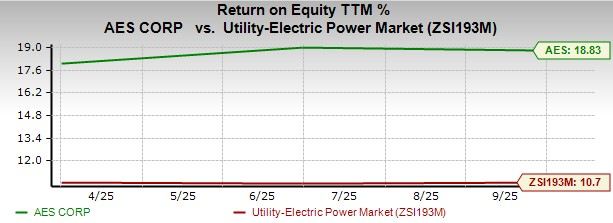

Return on Equity Outpaces Industry

AES has achieved a trailing 12-month return on equity of 18.83%, well above the industry average of 10.7%. This metric demonstrates the company’s effective use of shareholder capital to generate profits.

Investment Perspective

AES is capitalizing on the global shift toward renewable energy by investing in large-scale clean energy projects and energy storage, positioning itself for long-term growth. The company is also benefiting from surging demand from data centers, driven by AI and cloud computing, by securing long-term power purchase agreements for its renewable output.

While wholesale electricity prices have trended downward due to increased renewable supply, low natural gas prices, and demand management, which has led to lower rates for new renewable contracts, this trend could pose challenges for AES’s financial results.

Conclusion

AES remains a leader in the utility sector’s transition to clean energy, focusing on sustainable expansion, innovation, and strong financials. As the world moves toward carbon neutrality, AES continues to grow its renewable generation portfolio. With its projected earnings growth, strong return on equity, superior stock performance, and attractive valuation, AES may be a compelling addition for investors seeking exposure to the clean energy transition.

Additional Investment Insights

A lesser-known semiconductor company is emerging as a key player in the industry, offering products not produced by giants like NVIDIA. Positioned for the next phase of market growth, this company is just starting to gain attention.

With robust earnings and a growing customer base, it is well-placed to meet the increasing demand for Artificial Intelligence, Machine Learning, and the Internet of Things. Global semiconductor manufacturing is forecast to surge from $452 billion in 2021 to $971 billion by 2028.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Nelnet (NNI) Q4 Preview: Key Information Before Earnings Release

Bitcoin Gains Global Ground Despite Stagnant Valuation

AI Disruption Fears Prompt Scrutiny in Booming Secondary Market