Breaks Through 6.85! How to Understand the Strong Rally of the RMB?

The Renminbi continued its strong momentum at the beginning of the Year of the Horse. On February 26, both the onshore and offshore rates broke above the 6.85 mark, reaching their highest levels since April 2023. This round of appreciation is not only significant in magnitude but also demonstrates remarkable sustainability. The Renminbi has risen for seven consecutive months, marking the longest streak of gains since 2020. Since its bottom at the end of 2025, it has appreciated by 6.9%, and by 2.1% so far this year.

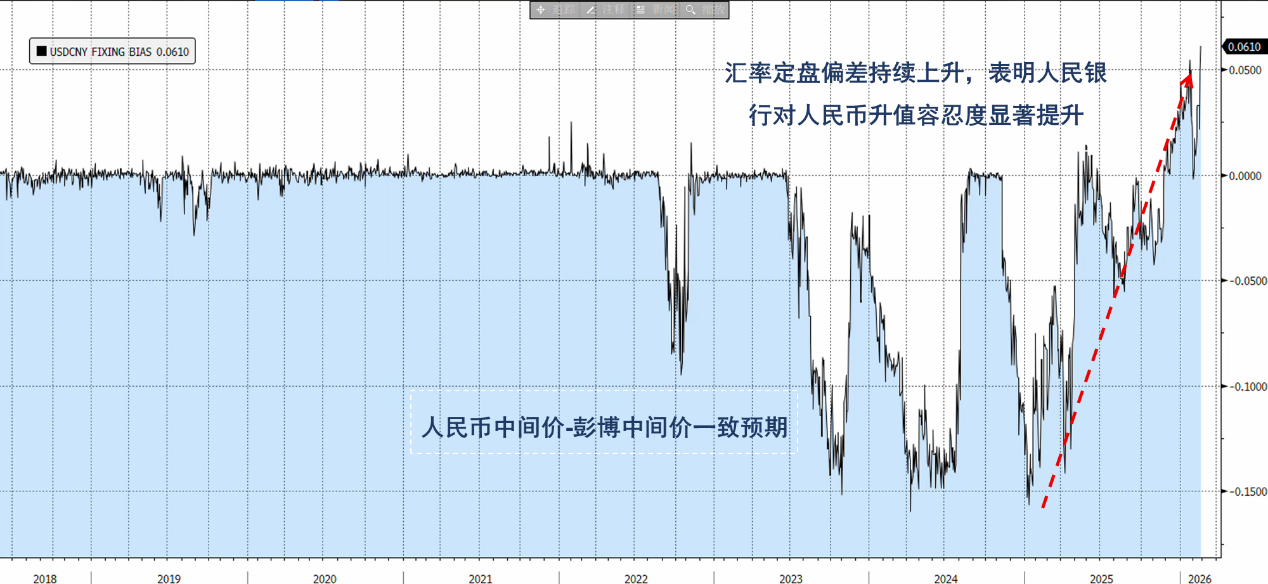

From market performance, this round of appreciation is characterized by a weak US dollar, amplified corporate foreign exchange settlements, and accommodating central bank policies: Firstly, it is a passive appreciation against the backdrop of a continuously falling US dollar index; secondly, exporters have concentrated on foreign exchange settlements around the year-end and Spring Festival, releasing previously accumulated US dollar positions and boosting short-term supply; thirdly, the continued strong bias in the central parity rate setting shows that regulators have increased tolerance for the gradual appreciation of the Renminbi.

As the Renminbi has strengthened for several consecutive months and shown stronger-than-expected performance beyond seasonal patterns, the market is highly concerned about whether the appreciation trend can continue. Although the risk reversal indicator in the options market is currently rising, with the 1-month USD/offshore RMB risk reversal reaching 0.43%, indicating that some traders have started to hedge downside risks, the overall trend still favors Renminbi appreciation.

Limited Impact of Dual Pressures from Renminbi Appreciation, Boost to Internationalization Process

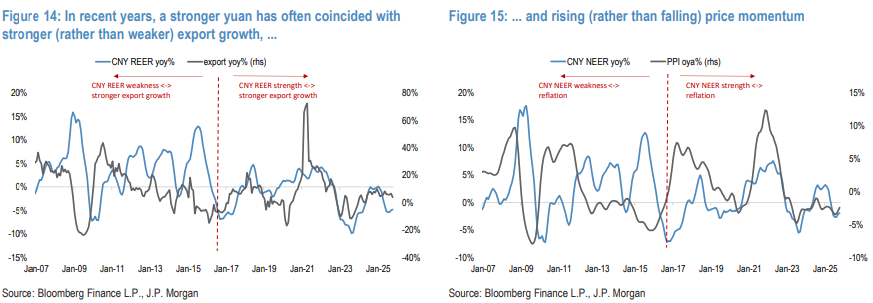

Although the market generally worries that Renminbi appreciation will weaken China’s export competitiveness and drag on economic recovery, such textbook concerns are not significant in China. Nominal exchange rate appreciation does not contradict strong export growth. Since 2017, Renminbi strength has often been accompanied by stronger exports and a rebound in price momentum. From 2021 to 2025, the Renminbi appreciated by only 3% against a basket of currencies, while exports increased by 44.8%.

Moreover, China’s shift towards a higher-tech and higher value-added export structure has reduced its sensitivity to exchange rates, as these products have lower substitutability. This year, the market consensus expects a 3% appreciation in the nominal effective exchange rate (NEER) and a 1.5% appreciation in the real effective exchange rate (REER), which will only drag down actual GDP growth in 2026 by 10 basis points. Therefore, the actual drag from appreciation on exports and economic growth is very limited.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Krispy Kreme: Fourth Quarter Financial Overview

Viatris: Fourth Quarter Financial Overview

Rising Middle East tensions lift gold as capital flight to safety continues