Sirius XM: Hidden Gem or Declining Investment?

Sirius XM: Evaluating Competitive Strength and Future Prospects

Investors considering Sirius XM face a fundamental question: does the company have lasting advantages that can deliver sustained value, or is it on a downward trajectory? Current data suggests Sirius XM has limited competitive strength and is experiencing structural challenges, leading to considerable uncertainty about its future.

While Sirius XM boasts a recognizable brand and a dedicated customer base, earning it a Narrow Moat rating, its advantages in distribution and pricing are increasingly threatened by the rise of streaming competitors. Rather than expanding its market position, the company is now focused on defending its existing share.

The most telling sign of these difficulties is the decline in its core subscribers. In 2025, Sirius XM reported a drop of 301,000 paid subscribers over the year. Although the overall subscriber count has remained relatively stable, it is still about 1% lower than the previous year. This gradual loss of paying customers, despite a slight improvement in monthly churn, signals stagnation in user growth. Revenue has mirrored this trend, remaining flat for the quarter and falling 2% year-over-year.

The company's strategy for increasing free cash flow is central to its value proposition. Sirius XM aims to reach $1.5 billion in free cash flow by 2027, a 19% rise from the $1.26 billion achieved in 2026. This goal is supported by reduced satellite capital spending. To justify its valuation, Sirius XM must grow cash flow faster than its subscriber and revenue declines. If cash flow growth only compensates for losses elsewhere, the stock may prove to be a value trap.

Analyzing Free Cash Flow, Dividend Yield, and Investment Safety

The investment rationale for Sirius XM boils down to whether its cash generation is sufficient to offset the ongoing decline in its business. Strong cash flow supports a high dividend yield, but the company's trajectory raises questions about long-term sustainability.

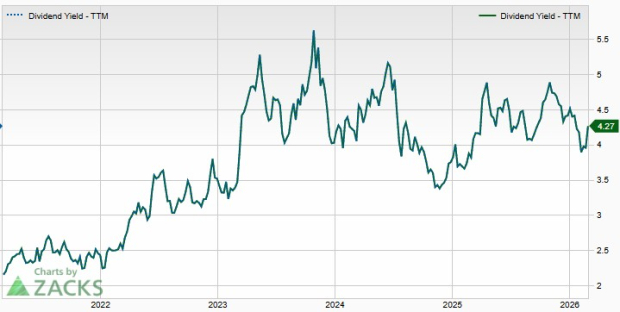

One of Sirius XM's notable strengths is its ability to pay substantial dividends. The board recently announced a $0.27 per share quarterly dividend, equating to a yield of around 5%. This payout is well-supported, with free cash flow in the first nine months of 2025 far exceeding dividend expenses. For investors seeking income, this provides a tangible return while waiting for a possible recovery or revaluation.

Despite these strengths, the stock's valuation reflects significant skepticism. Over the past five years, shares have dropped more than 60%, and the current P/E ratio of 7.33 indicates the market expects continued deterioration. This low valuation underpins the value argument, suggesting investors are not optimistic about the company's cash generation beyond the near term.

Assessing the margin of safety involves comparing the stock price to a reasonable estimate of intrinsic value. According to Morningstar, Sirius XM's fair value is $31 per share. With the current price near $22, this represents a roughly 30% discount. However, Morningstar also assigns a 'Very High' uncertainty rating, highlighting the difficulty of predicting outcomes for a company losing its core subscribers while trying to boost cash flow.

In summary, while the numbers provide some cushion, they do not guarantee safety. The dividend is well-covered, and the stock trades at a significant discount. Yet, the high uncertainty rating underscores the risk posed by the company's ongoing decline. For value investors, the margin of safety depends not just on the discount, but also on the strength of the company's competitive moat. Sirius XM's narrow moat and structural challenges mean the safety net is less robust than it appears.

Looking Ahead: Catalysts, Risks, and Key Metrics

Sirius XM's future depends on the interplay between management's efforts to stem subscriber losses and the continued erosion of its core business. The outcome will determine whether the stock's current discount is a temporary opportunity or signals a lasting downturn.

One potential catalyst is the success of new, lower-priced subscription options. Initiatives such as SiriusXM Play, an ad-supported tier, and Companion Plans are designed to retain customers and slow subscriber decline. If these strategies can stabilize the user base, they may help support revenue and achieve ambitious cash flow targets. However, these alternatives may also reduce average revenue per user (ARPU), creating a trade-off between subscriber numbers and profitability.

The main risk is that ongoing declines in subscribers and revenue will undermine the company's foundation, even if free cash flow grows. Management's improved guidance for 2025 showed better-than-expected results for revenue and EBITDA, but both were still lower than the previous year. The core challenge is structural: Sirius XM is a traditional business facing long-term decline and competitive disadvantages against streaming platforms. If new strategies fail to gain traction, the erosion of the user base will persist, making it difficult to justify the current valuation over the long term.

Adding complexity is the company's significant ownership by Berkshire Hathaway, which holds over 37% of outstanding shares. The rationale behind this investment is not fully transparent. While Berkshire's continued stake suggests confidence in intrinsic value, it does not guarantee a near-term catalyst or clear exit plan. This concentrated ownership means the stock's direction may be influenced by decisions from a single, long-term investor whose intentions are not publicly disclosed.

For value investors, the essential factors to monitor are the trend in self-paying subscribers and the effect of new pricing tiers on ARPU. It is crucial to track whether free cash flow growth can consistently outpace revenue declines, which is necessary for the current stock price to remain justified. The dividend yield offers a tangible return, but the potential for long-term growth depends entirely on whether Sirius XM can stabilize its business or continues to contract.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Keep An Eye on These 4 Bank Stocks With Recent Dividend Hikes

Keep An Eye on These 4 Bank Stocks With Recent Dividend Hikes

Pfizer Stock: Buy, Sell or Hold After Its 11% Rally So Far in 2026?