Macroeconomic Repricing Amid US-Iran Conflict: Will the 1970s Stagflation Crisis Repeat?

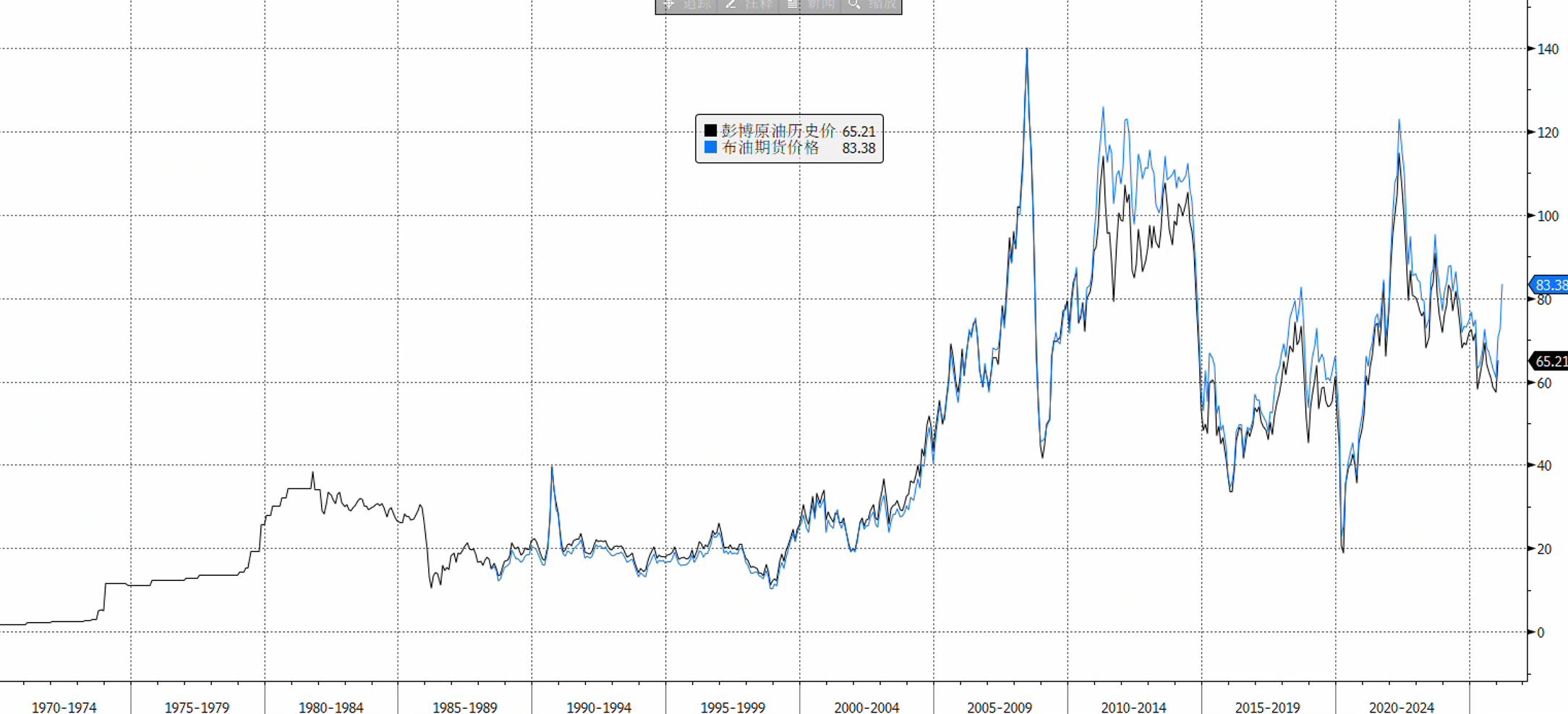

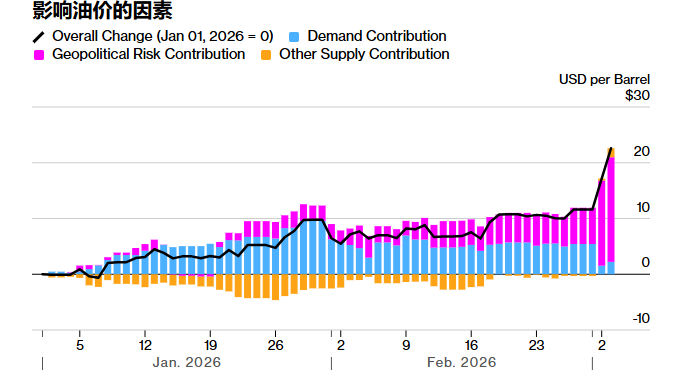

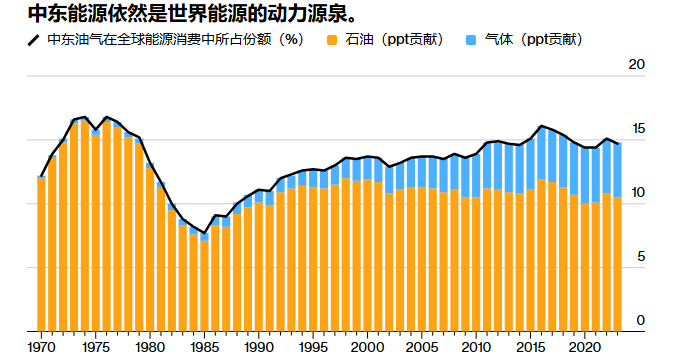

With the escalation of the US-Israel-Iran conflict, shipping in the Strait of Hormuz has been significantly hampered, putting about 20% of global crude oil and LNG supply at risk of disruption. Brent oil prices have surged quickly above $80, while diesel, shipping rates, and war risk insurance costs have all spiked in tandem. The crack spread in energy prices has widened, reflecting an increasingly tight supply of refined oil products. Currently, the market is repeatedly pricing between scenarios of short-term military friction and long-term strategic blockade, making inflation expectations and the path of the Federal Reserve’s policy the core variables.

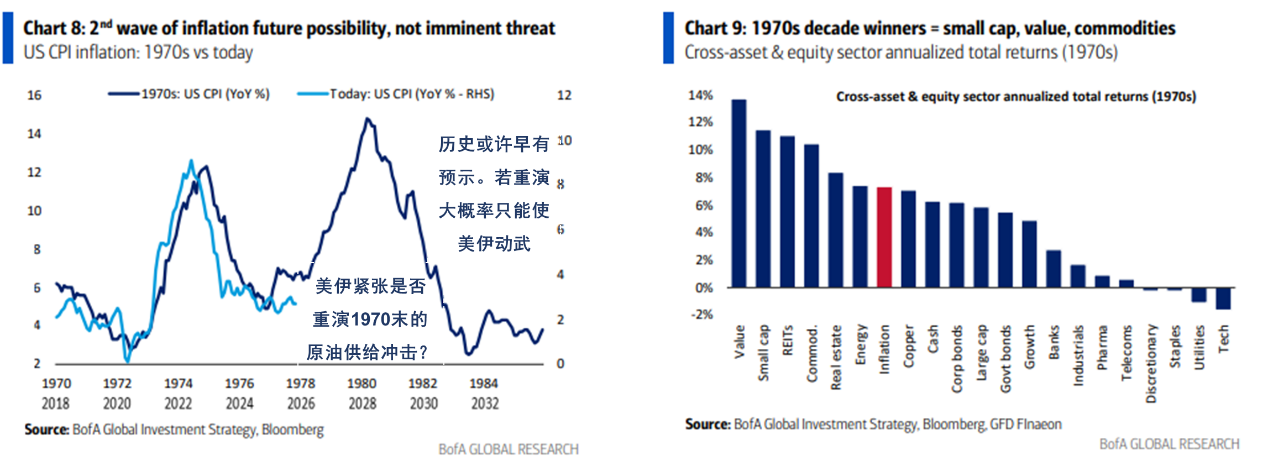

Looking back at history, the Fourth Middle East War and oil embargo in 1973, as well as the Iranian Revolution and the Iran-Iraq War in 1979, triggered global energy supply shocks twice: Oil prices doubled within months, the US CPI surged into double digits, the US stock market saw deep pullbacks, and real bond yields experienced dramatic swings. Afterwards, under the aggressive tightening policy led by then Federal Reserve Chair Paul Volcker, the US suppressed inflation at the cost of high unemployment and deep recession, barely managing to survive the stagflation crisis. The key question now for the market is whether this round of conflict meets the macroeconomic conditions to repeat the stagflation chain reaction of the 1970s.

In our coverage on January 29, "Crude Oil Volatility: US-Iran Geopolitical Risks Return to Pricing Core," we noted that "currently, low oil prices and high inventories have significantly decreased concerns about energy inflation within the US, thus lowering the costs of limited, surgical strikes. The current level of oil prices does not impose obvious pressure on US inflation or the cost of living for Americans, which decreases US concerns about the consequences of high oil prices in Middle Eastern affairs, making it more willing to take aggressive steps on sanctions and military deterrence."

However, this time, the US carried out surgical strikes on Iranian leaders, but unlike the quick end to the crisis following the surprise attack on Venezuelan President Maduro, the conflict has not ended swiftly, and Iran has declared itself prepared for a prolonged war. Meanwhile, the reaction of US stocks to this round of conflict has remained mild, implying that the market has not yet fully priced in the risks of a prolonged blockade of the Strait of Hormuz. This mild reaction is not a coincidence, but conforms to the usual pattern of market response: Only when a geopolitical event spills over to affect other macro variables such as economic growth or inflation does the market respond in a persistent and broad manner; lacking such economic spillovers, the impact typically remains confined to directly affected assets and rarely spreads further (see the January 8 article "What Conditions Are Needed for Geopolitical Tensions to Cause Significant Market Reactions?").

However, some Asian economies such as Japan and South Korea are more vulnerable to the closure of the Strait of Hormuz. Combined with strong prior momentum trends, investors have taken profits as risk aversion has risen, resulting in large capital outflows and triggering stampede-style sell-offs. The impact on European markets has also been more severe than in the US, as they are more affected by surging crude oil and natural gas prices, resulting in sharper market reactions than in the US market.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

OpenAI’s Super Bowl Prank: Evaluating the Reality Behind Hardware Speculation

Analyst to XRP Holders: Block All Moonboys Calling for $1000. Here’s why

USD/CHF declines as the US Dollar eases from its highest levels in months