Should You Purchase or Retain Dollar General Before the Fourth Quarter Earnings Announcement?

Dollar General Set to Announce Q4 Fiscal 2025 Results

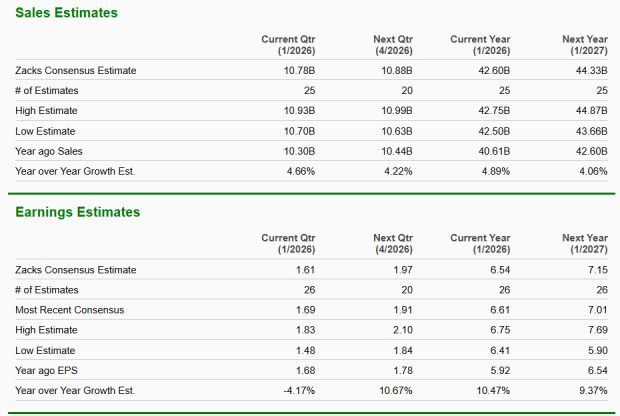

Dollar General Corporation (DG) is scheduled to unveil its fourth-quarter fiscal 2025 earnings before markets open on March 12. Investors are expected to focus on metrics such as store traffic, same-store sales, and profit margins.

While revenue is anticipated to rise, net income may decline. Current analyst projections estimate sales at $10.78 billion, marking a 4.7% year-over-year increase. The consensus for earnings per share has edged up by $0.04 in the past month to $1.61, but this still represents a 4.2% drop compared to the prior year. Over the last four quarters, Dollar General has averaged a 22.9% earnings surprise, with the most recent quarter exceeding expectations by 39.1%.

Source: Zacks Investment Research

DG Earnings Outlook According to Zacks

As Dollar General prepares to report its quarterly results, many are wondering if the company will surpass earnings forecasts. According to Zacks’ predictive model, Dollar General is likely to deliver an earnings beat this quarter. The combination of a positive Earnings ESP and a Zacks Rank of #3 (Hold) increases the probability of outperformance. Dollar General’s Earnings ESP stands at +5.38%.

Price, Consensus, and EPS Surprise for Dollar General

Key Drivers for Dollar General’s Q4 Performance

Dollar General’s results are expected to benefit from its focus on value, which continues to attract shoppers facing economic challenges. The company’s commitment to low prices and a broad selection of affordable products appeals to cost-conscious consumers. By maintaining a significant price advantage, Dollar General strengthens its reputation and increases store visits, especially among lower and middle-income customers seeking convenience and savings.

Market share gains in both consumable and non-consumable categories have fueled positive sales trends across essentials, seasonal items, home goods, and apparel. Efforts to expand product variety, bolster private labels, and improve category management are resonating with shoppers. Enhanced seasonal offerings and improved merchandising displays have likely contributed to higher traffic and same-store sales, with a projected 2.8% increase for the quarter.

Expansion and remodeling initiatives, including Project Renovate and Project Elevate, continue to refresh stores and optimize layouts, enhancing the shopping experience and boosting productivity. Dollar General is also advancing its digital strategy, expanding myDG Delivery for faster shopping. The same-day delivery service, available via the DG app and website, leverages the company’s extensive store network to provide quick access to essentials, particularly in rural areas. Partnerships with DoorDash and Uber Eats further support this convenience-driven approach.

However, profitability may be challenged by cautious consumer spending and rising operational costs. Shoppers are buying fewer items per visit, limiting basket growth. Increased expenses for store operations, maintenance, and utilities could pressure margins. Despite constructive sales trends, these factors may restrain earnings for the quarter.

Dollar General’s Stock Performance

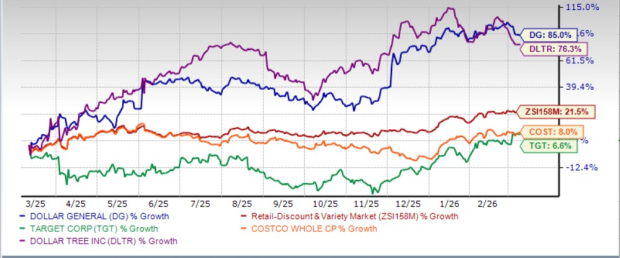

Over the past year, Dollar General shares have soared 85%, outpacing the industry’s 21.5% gain. The company has outperformed rivals such as Target Corporation (TGT), Costco Wholesale Corporation (COST), and Dollar Tree, Inc. (DLTR). Dollar Tree’s stock jumped 76.3%, while Costco and Target saw increases of 8% and 6.6%, respectively.

Source: Zacks Investment Research

Is Dollar General a Good Value Investment?

Dollar General currently trades at a forward 12-month price-to-earnings (P/E) ratio of 20.17, which is below the industry average of 33.31 and the S&P 500’s P/E of 21.84. However, the stock is priced above its one-year median P/E of 17.61. Compared to peers, Dollar General’s valuation is higher than Target (15.01) and Dollar Tree (17.09), but lower than Costco (47.18).

Source: Zacks Investment Research

Should Investors Buy or Hold Dollar General?

Dollar General’s strong value proposition, expanding store network, and growing digital initiatives position it for continued sales momentum. However, persistent margin challenges and cautious consumer behavior may limit earnings growth. Given the stock’s impressive performance and a mix of positive fundamentals and potential risks, investors might prefer to wait for the upcoming earnings report before making new investment decisions. Current shareholders may benefit from holding their positions, while new investors could seek more clarity from management’s commentary.

AI Investment Opportunities Beyond Nvidia

The artificial intelligence boom has already created significant wealth, but lesser-known companies addressing major global challenges may offer greater upside in the future.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Will RIVER crypto drop to $7.72 next as short leverage rises?

Q4 Financial Results Overview: Cognex (NASDAQ:CGNX) Compared to Other Specialized Technology Equities

Q4 Top Earnings Performers: Texas Capital Bank (NASDAQ:TCBI) And Other Regional Bank Stocks

Manulife's Strong Core Profits Overlooked as Market Bias Leaves Shares 10% Below Value