Chinese Economy Shows Unexpected Recovery, Yet Threats of Conflict Remain

China's Economy Sees Early 2026 Surge Amid Global Uncertainty

China experienced a notable economic revival at the start of 2026, with domestic spending and investment both exceeding expectations. However, ongoing conflict in Iran threatens to disrupt exports, casting doubt on the sustainability of this momentum.

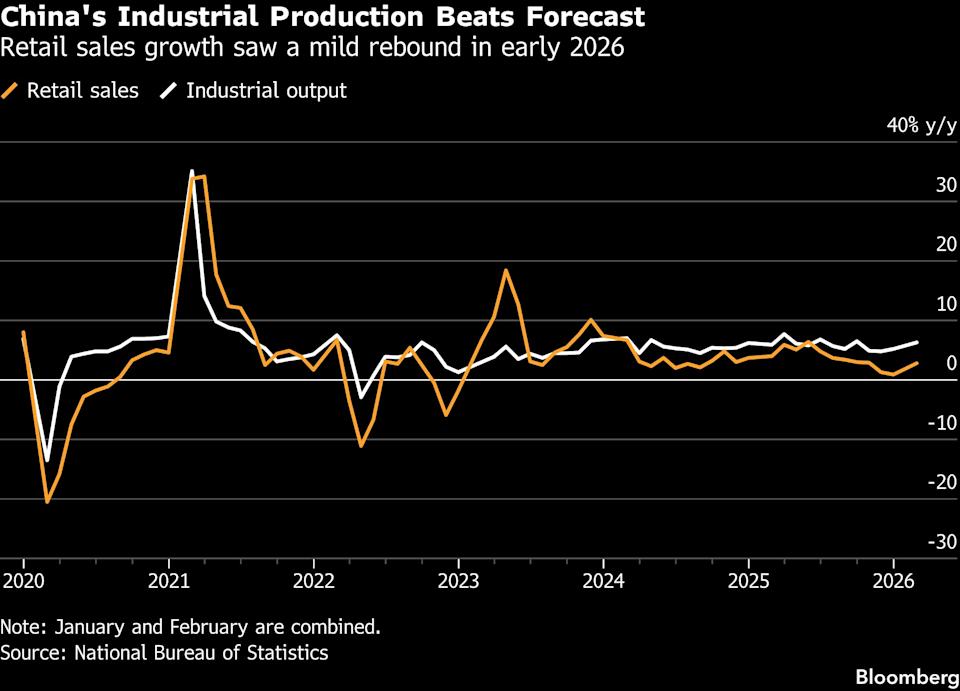

Manufacturing activity picked up pace as overseas shipments increased sharply in the opening months of the year. According to the National Bureau of Statistics, industrial production grew by 6.3% in January and February compared to the previous year, marking the fastest expansion since September.

Trending Stories from Bloomberg

Other sectors driven by local demand also outperformed forecasts. Retail sales jumped 2.8% over the first two months—more than three times December’s growth—while fixed-asset investment unexpectedly rose by 1.8%, reversing last year’s historic decline.

Despite mounting geopolitical risks and volatility in global trade and energy markets, the latest data suggests China began the year on a stronger footing than anticipated. Hao Zhou, chief economist at Guotai Junan International, noted that this resilience could help buffer the economy from external shocks in the short term.

These figures offer a positive snapshot for the world’s second-largest economy, which ended 2025 with its slowest growth since emerging from pandemic restrictions in late 2022. As consumer spending and investment cooled, GDP growth slowed to 4.5% year-on-year in the fourth quarter.

However, recent escalation in the Middle East has unsettled energy markets and disrupted trade flows. While China is less exposed to oil price spikes than some Asian peers, its export sector remains vulnerable to global economic headwinds and inflationary pressures.

Rising costs for energy and raw materials could further erode manufacturers’ profits, especially amid fierce competition.

Following the upbeat economic data and a surge in oil prices due to the Iran conflict, Chinese government bonds saw yields rise, with the 30-year bond yield reaching its highest level since August 2024. The offshore yuan also held onto a modest gain against the US dollar.

Policy Outlook and Investment Trends

The broad-based improvement in economic indicators may prompt policymakers to hold off on new stimulus measures as they monitor the evolving situation in the Middle East. While economists surveyed by Bloomberg in February anticipated interest rate and reserve requirement cuts by the end of March, the likelihood of such moves being delayed is increasing.

Serena Zhou, senior China economist at Mizuho Securities, highlighted the unexpected rebound in fixed-asset investment as a key surprise, suggesting it could postpone the anticipated rate cut.

Previously, China’s investment had been shrinking month-over-month since mid-2025, attributed to waning business confidence, possible statistical adjustments, and a slowdown in government infrastructure spending as debt repayment took priority.

Now, a shift appears underway: infrastructure investment soared 11.4% year-on-year in the first two months, the fastest pace since 2021. This surge may reflect the launch of projects delayed from late 2025, when growth targets seemed within reach.

Economists at CF40, a Beijing think tank, noted that the rapid recovery in infrastructure spending demonstrates proactive macroeconomic support and suggests fiscal stimulus will remain robust.

Manufacturing investment also rebounded, increasing by 3.1%. The rise in raw material prices, particularly for non-ferrous metals like copper, contributed to this turnaround.

Producer price declines have narrowed in recent months and could return to positive territory as early as March, buoyed by higher oil prices. A sustained price increase would support investment, which had been weighed down by deflation in recent years.

Still, Xue from Mizuho cautioned that it is premature to conclude whether real demand is truly recovering.

Consumer Spending and Government Policy

China typically combines January and February data to offset distortions from the shifting Lunar New Year holiday. A closer look at retail figures shows that demand for alcohol, cigarettes, communication devices, and jewelry drove growth, while car sales continued to decline.

Questions remain about the durability of the consumer recovery. The government has reduced subsidies for consumer goods purchases to 250 billion yuan ($36 billion) for 2026, down from 300 billion yuan in 2025, and is maintaining only modest increases in basic pension payments.

This year, Beijing set its economic growth target at 4.5%-5%, the least ambitious since 1991, though from a much larger GDP base. While exports were unexpectedly strong early in 2026, the outlook now depends in part on how long and intense the conflict in Iran becomes, following US and Israeli strikes that began on February 28.

Bloomberg Economics Commentary

“Investment outperformed expectations, and consumption grew slightly faster than forecast. However, the relatively modest pace compared to historical standards highlights the challenges ahead for a robust recovery.”

— Chang Shu and Eric Zhu

Government Response and Future Prospects

So far, Chinese authorities have taken a measured approach, opting to observe developments rather than introduce sweeping new policies. Earlier this month, a slightly reduced fiscal stimulus plan was announced for the year.

While Chinese leaders have a track record of meeting their economic targets, achieving this year’s more modest goal will be closely watched. The country’s increasing dependence on exports is straining relations with trade partners and has yet to deliver significant benefits to households.

The National Bureau of Statistics commented, “In January and February, key economic indicators showed a clear rebound and a strong start to the year. However, we must also recognize that the impact of external changes is deepening and geopolitical risks continue to rise.”

Most Read from Bloomberg Businessweek

©2026 Bloomberg L.P.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

El.En. Smart Money Wonders: Can the €172M Cash Cushion Fund Dividends While Profits Shrink?

WDAY or IBM: Which Enterprise Software Company Is the Superior Investment Choice Today?

Pre-market rises as oil prices cool and new data emerges

Bitcoin Depot Inc. (BTM) Posts Fourth Quarter Loss, Surpasses Revenue Projections