Microsoft Copilot Set to Redefine Office Work—As AI Moves From Tool to Operating System

We are witnessing the dawn of a new compute layer for the office. Generative AI is not merely a tool to be added to existing workflows; it is the foundational infrastructure that will redefine how knowledge work gets executed. This is a paradigm shift, comparable in scale to the internet's arrival decades ago. The companies building these fundamental rails are the developers of the foundational models-Anthropic, OpenAI, Google, and others-whose large language models provide the raw cognitive power. Then there is the integrator, MicrosoftMSFT+1.05% Copilot, which is embedding this new compute layer directly into the operating system of the modern office suite.

The adoption curve for this new layer is still in its early, slow phase. Data shows that only 38% of organizations have integrated AI tools to improve productivity, while a striking 49% of workers report never using AI in their role. This gap between corporate investment and frontline adoption is the hallmark of a technology on the lower slope of the S-curve. The McKinsey report notes that while 92 percent of companies plan to increase AI investments, only 1% of leaders consider their deployment mature. The transformation is long-term, with the potential to add $4.4 trillion in productivity, but the path from promise to pervasive integration is measured in years, not quarters.

For now, the impact is incremental. AI is nibbling at the edges of the office, automating repetitive tasks in spreadsheets and drafting documents, as noted in recent commentary. This is the predictable, structured work that serves as the "candy" for the new compute layer. The real shift will come when this infrastructure becomes as essential and invisible as electricity or the internet was for the last industrial revolution. The companies that build the most robust, reliable, and deeply integrated rails will define the next era of work.

The Exponential Payoff: Productivity Gains and the Maturity Gap

The promise of AI is an exponential payoff in productivity, but the path to realizing it is defined by a stark maturity gap. Early evidence shows dramatic task acceleration. Research from Anthropic found that typical workplace tasks take about 90 minutes without AI, but tools like Claude can speed them up by about 80%. Extrapolating this, researchers suggest current models could boost US labor productivity growth by 1.8% annually over the next decade-roughly double the recent run rate. This is the kind of acceleration that signals a paradigm shift, moving work from a linear to a non-linear curve.

Yet the long-term potential is even more staggering. McKinsey research sizes the total opportunity at $4.4 trillion in added productivity growth from corporate use cases. This isn't incremental improvement; it's a fundamental redefinition of economic output. The gap between this potential and today's reality is the maturity gap. While 92 percent of companies plan to increase AI investments, only 1 percent of leaders consider their deployment mature and fully integrated into workflows. This statistic is the key metric. It shows we are still in the early, adoption-heavy phase of the S-curve, where investment is high but the infrastructure is not yet woven into the fabric of daily operations.

| Total Trade | 12 |

| Winning Trades | 7 |

| Losing Trades | 5 |

| Win Rate | 58.33% |

| Average Hold Days | 16.08 |

| Max Consecutive Losses | 2 |

| Profit Loss Ratio | 1.34 |

| Avg Win Return | 2.59% |

| Avg Loss Return | 1.84% |

| Max Single Return | 3.91% |

| Max Single Loss Return | 4.46% |

This creates a financial puzzle. The early gains are real, but the long-term payoff hinges on replacement economics-whether AI can truly displace human labor at scale. The evidence suggests this is unclear. A recent study found that while AI tools speed up work, they often intensify it, leading to task expansion, cognitive fatigue, and longer hours. Workers take on broader scopes, blurring work-life boundaries. This may boost output in the short term, but it risks burnout and unsustainable workloads, undermining the very productivity gains sought. The financial feasibility of widespread replacement, therefore, remains an open question. The exponential payoff is real, but it will only be captured when companies successfully navigate the maturity gap and build systems that amplify human agency without degrading it.

The Diffusion Challenge: Scaling Adoption and Workforce Impact

The infrastructure is being built, but the real test is diffusion-the spread of this new compute layer across the entire economy. Right now, adoption is a story of extreme concentration. The key metric is stark: almost 90% of all AI-related job postings came from just 1% of companies in 2025. This is the diffusion challenge in its purest form. The economic benefits of AI are currently accessible only to a tiny, elite subset of firms, raising serious concerns about uneven economic diffusion. While the share of firms with AI job postings has tripled since 2018, the growth has been heavily skewed toward the largest players. This creates a two-tier system where a small number of giants can capture the productivity payoff, while the vast majority of businesses lag behind, potentially widening existing productivity and competitive gaps.

This uneven spread is mirrored in the workforce impact. The signal from the largest firms is clear: AI is being deployed to replace human labor. Companies like HP and IBM have signaled they are replacing jobs with AI, and CEO Jack Dorsey announced that Block was eliminating approximately 40% of its staff. The MIT study cited earlier found that AI can already replace 11.7% of the US labor market, and the initial wave of corporate announcements confirms this is not a distant future but a present reality. Yet, this replacement economics creates a new tension. The very productivity gains that drive these decisions may be offset by a surge in overwork.

Real-world evidence shows AI tools intensify work, leading to task expansion and longer hours. A recent study from the University of California-Berkeley found that employees using AI worked at a faster pace, took on a broader scope of tasks, and extended work into more hours of the day. This is the productivity offset. Workers willingly take on more, spurred by the ease AI brings to individual tasks. The result is a faster, broader workload that can lead to cognitive fatigue, burnout, and ultimately, lower quality work. This dynamic undermines the sustainability of the initial productivity surge and poses a significant risk to the long-term financial model of AI-driven efficiency. The exponential payoff requires not just adoption, but a balanced integration that amplifies human capacity without degrading it. For now, the diffusion challenge and the risk of overwork represent the two major frictions that could slow the adoption curve from its current steep climb.

Catalysts and Watchpoints: The Path to Exponential Growth

The path from AI's current tool-like status to a true paradigm shift is defined by a few critical catalysts and watchpoints. The primary catalyst is a fundamental shift in usage: moving from isolated task automation to deep workflow integration. Right now, the promise is often about getting more employees to use AI for specific jobs, like drafting documents. The exponential payoff requires this to evolve into embedding AI directly into the core processes of business, where it doesn't just assist but redefines how work flows from start to finish. This is the transition from a productivity tool to an operating system.

The key watchpoint is the evolution of hiring patterns. The data on job postings is a leading indicator of where strategic investment and adoption are concentrated. As of late 2025, almost 90% of all AI-related job postings came from just 1% of companies. This extreme skew is a red flag for uneven diffusion. For AI to drive broad economic growth, this pattern must change. Investors and business leaders should monitor whether the share of firms with AI job postings continues to rise, and crucially, whether that growth spreads beyond the largest players to medium and small businesses. If adoption remains the domain of a few giants, the aggregate productivity impact will be limited.

This brings us to the competitive inflection. The widening gap in productivity growth between early adopters and laggards is the ultimate signal of exponential growth taking hold. The McKinsey report notes that while 92 percent of companies plan to increase their AI investments, only 1 percent of leaders consider their deployment mature. This maturity gap is the current state of play. The inflection point will arrive when a significant cohort of firms crosses this threshold, achieving workflow integration that drives measurable, outsized business outcomes. The competitive landscape will then fracture, with AI-adopting firms pulling ahead on efficiency and innovation, while laggards face a growing cost disadvantage. The watchpoint is clear: track the adoption curve not just in terms of investment, but in terms of the tangible, integrated outcomes it produces.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Flow Review: MiCA’s Initial Year and the Dozen Banks Powering Crypto Market Liquidity

STMicroelectronics accelerates global adoption and market growth of Physical AI with NVIDIA

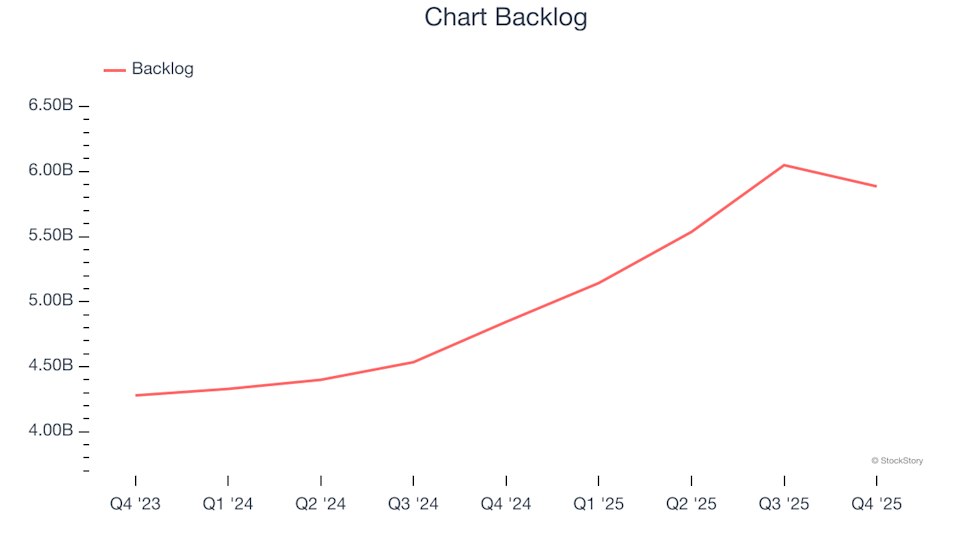

Chart (GTLS): 3 Factors That Make This Stock Attractive

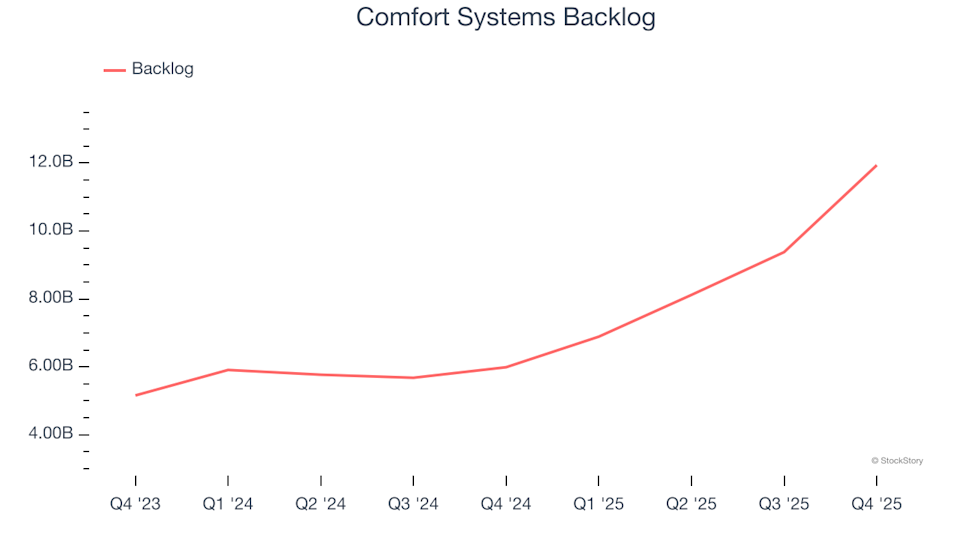

3 Reasons Why FIX Could Experience Significant Growth