Middle East Crisis Now the Main Character Driving FTSE 100’s 11% Correction and BoE Rate Hike Bets

The market's reaction to the Middle East crisis is no longer a whisper; it's a roar. The catalyst is clear, and its impact is quantified in sharp daily drops and surging energy prices. The FTSE 100's 2.75% drop yesterday was its worst single day in 11 months, a violent repricing that echoed across global indices. This wasn't an isolated event. The index has now fallen about 11% since the war erupted earlier this month, officially confirming it has entered correction territory.

The engine driving this sell-off is energy. The conflict has ignited a search for safe havens and a direct threat to supply, sending oil prices into a frenzy. Brent crude has jumped 12% over the first three days of the week and is now climbing toward $84 a barrel. This surge is more than a headline; it's a tangible cost shock that investors are pricing in. The market's attention is laser-focused on this viral sentiment, with every escalation in the region directly translating to a tick higher in the oil benchmark and a corresponding drop in equities.

The connection between the headline and the market's pulse is direct. As the conflict threatens to disrupt the Strait of Hormuz, a critical chokepoint for global oil, the search volume for terms like "Middle East war," "oil prices," and "FTSE 100" has spiked. This isn't just correlation; it's causation. The FTSE 100's slide from its record high is a direct function of the inflation and growth fears that this energy shock brings. The market's main character is now the Middle East crisis, and its volatility is the story that everyone is googling.

Market Attention & Secondary Catalysts: BoE Hikes and UK Borrowing

While the Middle East crisis is the clear main character driving the market's sell-off, other financial topics are being priced in as secondary catalysts. The energy shock is forcing a re-rating of both monetary policy and fiscal health, amplifying the overall pressure.

The Bank of England is now being priced for a more aggressive stance. As the conflict pushes energy costs higher, markets have sharply revised expectations. Yields on Britain's 10-year government bonds have surged to their highest level since 2008, reflecting a shift in the pricing of future rate hikes. The market now anticipates four BoE interest rate rises for this year, a sharp reversal from expectations of two rates in 2026. This is a direct response to the inflationary threat from oil, showing how the Middle East headline is overriding previous dovish sentiment.

At the same time, domestic economic data is flashing red. The UK government's borrowing situation has worsened. In February, the public sector deficit jumped to £14.3bn, the second-highest February figure on record. This surge, which came after a record surplus in January, highlights the fiscal strain from higher energy costs and delayed debt interest payments. It adds another layer of concern for investors already worried about demand destruction.

The market's reaction shows a nuanced split. The FTSE 100 fell 2.4% on the day, but the FTSE 250 was hit harder, tumbling 3.2%. This divergence suggests mid-caps may be more sensitive to the domestic policy shift and fiscal data, while the larger FTSE 100's decline is more directly tied to the global energy shock and its growth implications. The precious metal miners, a sector hit by lower gold prices, were the biggest drag, further illustrating how the crisis is hitting specific, vulnerable segments.

The bottom line is that the Middle East crisis is the dominant driver, but it's acting like a catalyst that accelerates and intensifies other existing pressures. The BoE hike expectations and soaring government borrowing are not independent stories; they are direct financial reactions to the same headline. In this environment, the market's attention is a single spotlight, but it's illuminating multiple risks at once.

Sector Impact & What to Watch: The Main Beneficiaries and Risks

The Middle East crisis is the clear main character, and its volatility is now dictating sector moves. The most exposed groups are the obvious ones: miners and energy stocks, which are leading the declines. The precious metal miners were the biggest drag on the FTSE 100, as gold sank more than 5% to a four-month low. This isn't about the sector's fundamentals; it's a direct function of the geopolitical risk that is overwhelming all other narratives. The sector's performance is now dominated by the threat to supply and the resulting flight to safety, not by earnings reports or production data.

The key watchpoints are the next moves in the conflict that could spike oil prices further. Traders are now focused on a US 48-hour deadline for Iran retaliation and any potential move to blockade Kharg Island, vital to Iran's oil exports. These scenarios represent the next potential catalysts for a violent repricing of energy and, by extension, the entire market. The market's attention is laser-focused on these specific, high-stakes developments.

Currency markets are also feeling the strain. The pound fell 0.5% against the dollar, showing how the crisis is introducing a new layer of volatility beyond equities. This currency move reflects the broader uncertainty and risk aversion, as investors seek stability elsewhere.

For now, the beneficiaries of the turmoil are hard to identify. The market's reaction is overwhelmingly negative, with all sectors trading in red. The setup is one of broad-based selling pressure, where the headline risk is the only story that matters. The main character is the Middle East crisis, and its continued escalation is the single factor that will determine whether the sell-off deepens or finds a pause.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

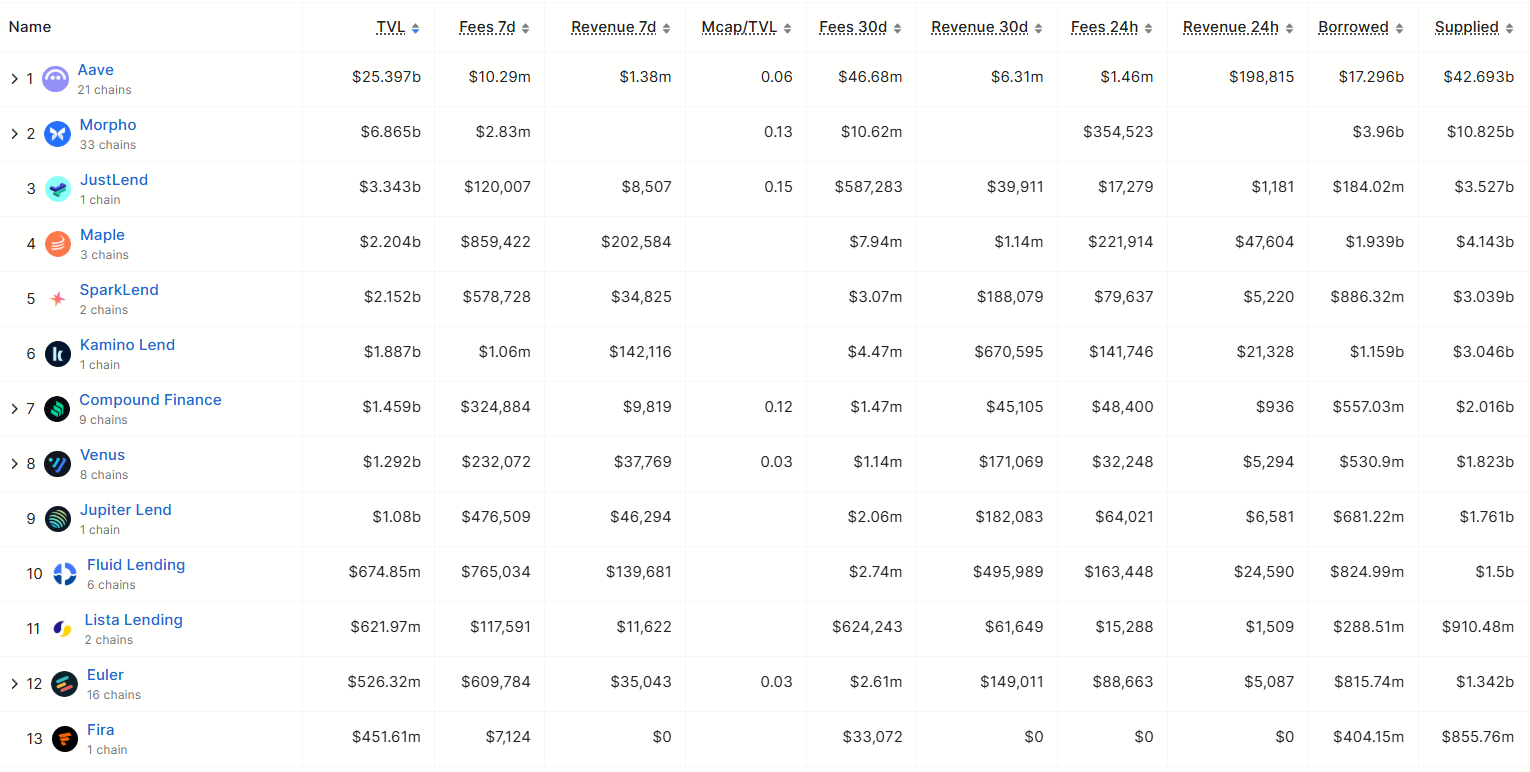

Fira launches fixed-rate DeFi lending market with $450M in deposits

TGEN Bounces Sharply—But No Catalyst in Sight